IDCFP’s CAMEL Ranks Explained - The “A” in CAMEL: Adequacy of Tier 1 Capital

IDC Financial Publishing, Inc. (IDCFP) uses the acronym CAMEL to represent the financial ratios used to evaluate the safety and soundness of commercial banks, savings institutions and credit unions. This article explains how IDCFP measures the adequacy of capital, the “A” component of its CAMEL ranks, and why it is valuable and important to monitor.

The “adequacy of capital” component of CAMEL measures the amount of adjusted Tier 1 capital. Tier 1 capital is adjusted by subtracting the amount of loan delinquencies (loans that are 90 days past due, nonaccrual loans, plus repossessed assets) in excess of loan loss reserves. An adjusted Tier 1 capital ratio below 5% indicates insufficient capital and loan loss reserves to cover loan delinquencies and results in an IDCFP rank less than 125.

IDCFP’s CAMEL ratings of banks, savings institutions, and credit unions range from 300 (the top grade attainable) to 1 (the lowest). From the early 1990’s, through today, institutions using our ranks determined that ratings lower than 125 were deemed below investment grade.

“A” Relative to Other CAMEL Components

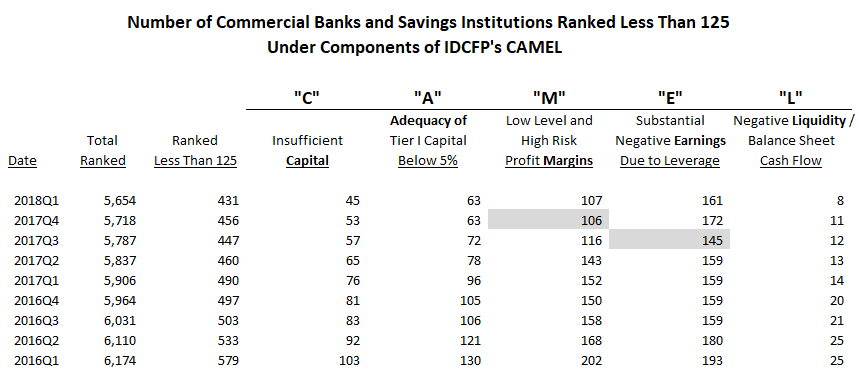

Although the total number of banks ranked less than 125 by IDCFP continues to decline, certain components of the CAMEL rating are exhibiting warning signs of risk to come. As shown in Table I, column “E,” more banks began exhibiting negative returns on financial leverage (ROFL) in 2017 Q4, resulting in negative earnings. In addition, there was a small increase in institutions yielding narrow profit margins with high standard deviations in this margin over time, shown in column “M.”

The other 3 components of IDCFP’s CAMEL are still declining or holding, indicating some time before a reversal and potential financial crisis. “C,” or institutions with capital that is deemed insufficient, is still declining, currently at 45. “A,” or institutions with less than 5% adequacy of capital, did not change from the previous quarter, holding at 63. Finally, “L,” or institutions with negative liquidity in balance sheet cash flow and substantial loan delinquency, is also still declining, currently at a level of 8 institutions (see Table I).

Table I

All 5 categories of rank, Capital, Adequacy of capital, Margins as a measurement of management, Earnings from operations and financial leverage, and, finally, Liquidity, together provide a timely indication of risk and potential failure. An increase in the number of banks ranked under 125 in all components of CAMEL is required to confidently forecast a future banking crisis.

Early Warning Indicators in History

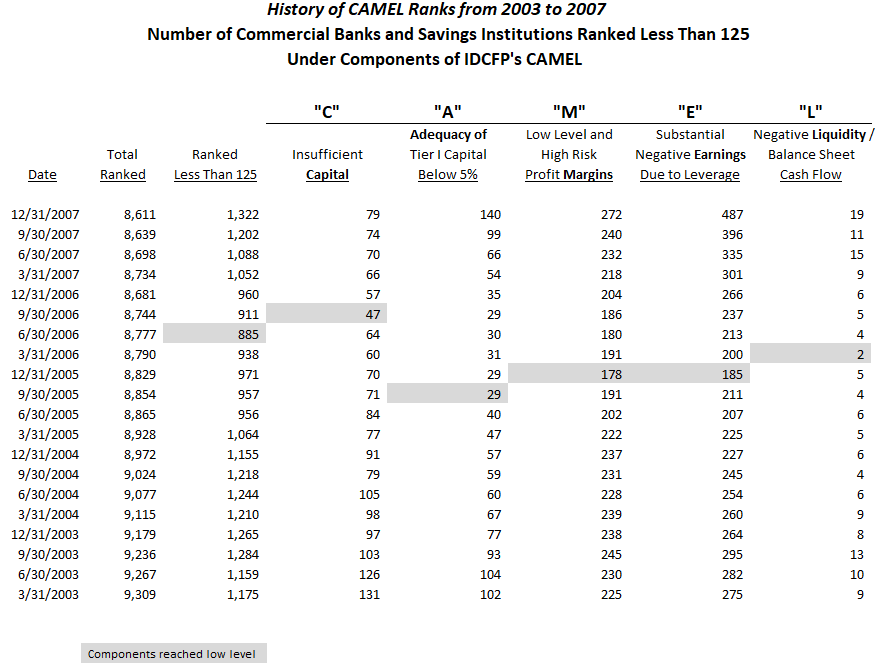

The number of commercial banks and savings institutions ranked below 125 reached a low in the 2nd quarter of 2006, two years before the banking crisis in 2008. More importantly, leading up to this point, 4 out of the 5 components of CAMEL also reached lows from the 3rd quarter of 2005 through the 1st quarter of 2006, and then began to rise.

As seen in Table II below, commercial banks and savings institutions with insufficient capital reached a low of 47 institutions in the 3rd quarter of 2006. Financial institutions with less than 5% adequacy of capital reached a low count of 29 in the 3rd quarter of 2005. Banks and savings institutions with a lack of profitability, or low and unstable margins, reached a low of 178 in the 4th quarter of 2005. The commercial banks and savings institutions with severe negative earnings due to financial leverage reached their low of 185 in the 4th quarter of 2005. Finally, institutions with high loan delinquency and negative balance sheet cash flow, or negative liquidity, reached their low of 2 in the 1st quarter of 2006.

Table II

As seen in history, the increase in the number of financial institutions with IDCFP’s CAMEL ranks below 125, or below investment grade, forecast the bank financial crisis a few years later. IDCFP’s ranks are critical for investors to monitor financial institutions.

For further information or to view our products and services please visit our website at www.idcfp.com or contact us at 800-525-5457 or info@idcfp.com.

John E Rickmeier, CFA

President

Robin Rickmeier

Marketing Director

IDC Financial Publishing, Inc.

700 Walnut Ridge Drive, Suite 201

PO Box 140

Hartland, WI 53029

P 800-525-5457

P 262-367-7231

F 262-367-6497