True Bank Cash Flow Profitability Versus Bank Estimated Stockholder ROE

On January 1, 2020, the Current Expected Credit Losses rule, or CECL, was imposed, which includes new guidelines for taking provisions for anticipated future loan losses. These guidelines require lenders to anticipate the losses today that they expect to incur on current borrowings in the future. As effects of the Covid-19 pandemic emerge, this type of long-term forecasting is becoming increasingly difficult, and probably led to CECL overestimating future loan losses.

In addition, banks by type have been allowed to decide when to implement CECL anytime from January 2020 to January 2023. Different implementation dates for CECL makes comparisons for reported income data and analyzing traditional return on equity (ROE) difficult between banks.

While IDC Financial Publishing (IDCFP) reports “stockholders return on equity” we also calculate “Net Operating After-Tax Return on Equity” (NOPAT ROE). Stockholder ROE is simply after-tax profits (after loan loss provision with or without CECL) divided by stockholder tangible equity. IDCFP’s NOPAT ROE is a cash flow-based ROE. The numerator equals NOPAT profits plus the increase in the loan loss reserve (loan loss provision greater than net charge offs), thereby reflecting actual loan losses. The denominator equals the stockholder tangible equity plus the loan loss reserve.

IDC Financial Publishing (IDCFP) measures relative profitability of bank holding companies by comparing the IDCFP return on tangible equity (NOPAT ROE) to our definition of the cost of equity (COE). Margin between ROE and COE (included in the “M” in IDCFP’s unique CAMEL analysis) is a key measure of management.

The Traditional ROE Equation

The traditional ROE equation simply divides net income by the average of common stockholder’s tangible equity capital. The stockholder ROE, as a bottom-line measure of profitability, fails to reflect the true cash nature of asset quality. In addition, the traditional components of this ROE ratio – net interest margin, net income return on assets (ROA), and resulting stockholder ROE – confuse the source of net income by subtracting cost of funding so early in the analysis. Managers are unable to separately compare operating and financial returns with their peers. Also, deduction of the loan loss provision, and not adjusting net income for the increase in the loan loss reserve, fails to reflect the true cash flow to earnings.

Our NOPAT ROE Equation

In contrast, the NOPAT ROE equation expresses ROE as a sum of two components. First is the return on earning assets (ROEA). ROEA focuses on operating strategy, which identifies after-tax returns from investments, loans, and noninterest income sources. It only reflects current net loan losses, adding back to the income increase in the loan loss reserve. The second component is the bank’s return on financial leverage (ROFL). This reflects both the degree to which the bank uses debt funds to finance its operating strategy and the after-tax cost of these debt funds.

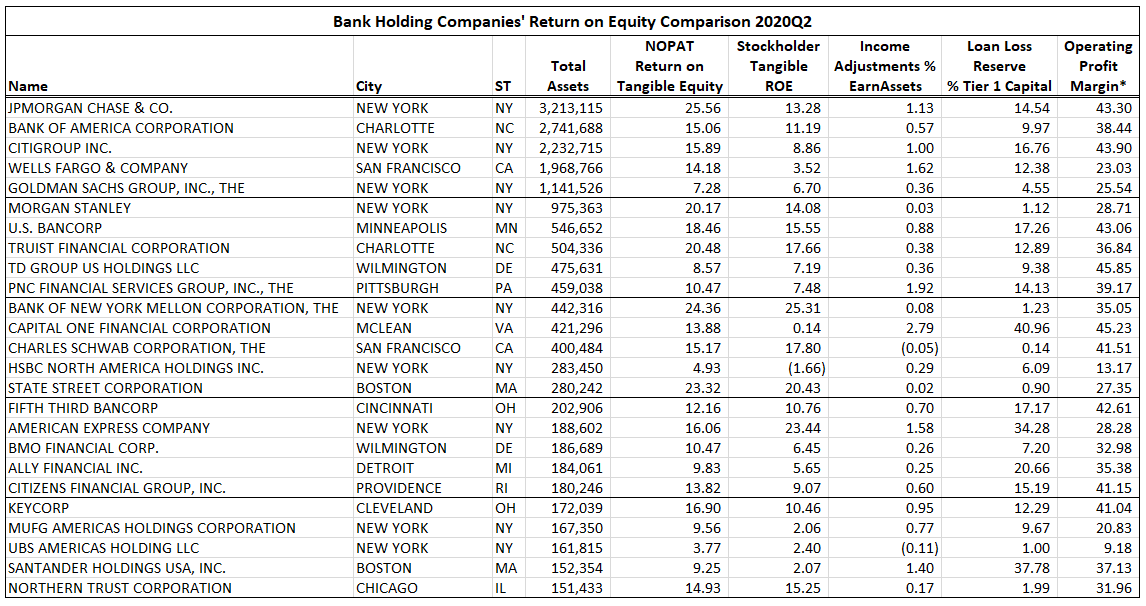

As an example, JP Morgan Chase & Co. reported a stockholder ROE of 13.3% for the second quarter of 2020. Our NOPAT ROE was 25.6%. The difference was mostly due to an income addition to ROEA of loan loss provision less net charge-offs equating to 1.13% of earning assets. The operating profit margin before loan loss provisions was an extremely high 43.3% (see Table I).

The 25 bank holding companies in the following table range from large to smaller regional institutions. These banks have operating profit margins from 45.9% to 9.2%, loan loss reserve % of Tier 1 capital from 40.1% to 0.1%, NOPAT ROE ranging from 25.6% to 3.8%, and total assets from $3,213 to $151.4 billion.

Table I

*Before loan loss provision

All reported financial data are from regulatory reports and accounting, not shareholder accounting.

Future Comparisons

A bank is allowed the loan loss provision adjustment to project future losses from current loans. IDCFP, on the other hand, computes the true cash flow NOPAT ROE that the bank earns, which is actual cash flow profitability. Given the potential errors in estimating CECL for the future of each existing loan at origination in the period of Covid, and the varied timetable for each bank to implement it, traditional ROEs are not comparable or reliable. IDCFP’s NOPAT ROE is a true reflection of cash-based earnings in today’s complicated economy.

To view all our products and services please visit our website www.idcfp.com.

For more information about our ranks, or for a copy of this article, please contact us at 800-525-5457 or info@idcfp.com.

John E Rickmeier, CFA, President, jer@idcfp.com

Robin Rickmeier, Marketing Director