Why Bank Stocks Outperform the S&P 500, Value, and Epicenter Stocks

Bank stocks benefit from accelerating earnings growth over the next few years due to 1) A secular rise in return in equity (ROE), and 2) The base of ROE, tangible book value per share (TBVPS), growing at 10% or more a year. A rising ROE with a 10% or more growth in TBVPS creates accelerating EPS growth well above Wall Street estimates.

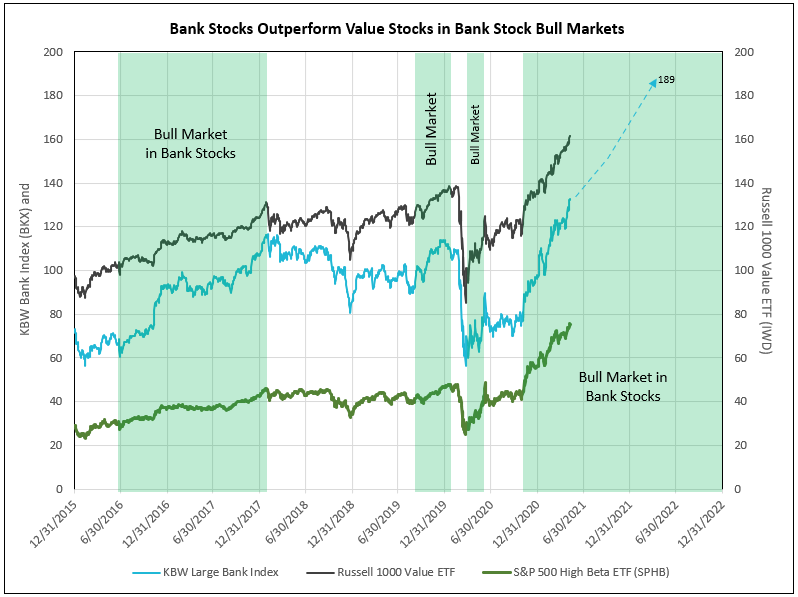

Bank stocks outperformed value stocks in the last three bank stock bull markets (06/30/2018 to 02/28/2019, 08/30/2019 to 12/31/2020, and 09/30/2020 to date). In all three bull markets, both German and U.S. 10-year yields rose on trend.

Chart I

The key to understanding the fundamentals driving the current bank stock bull market is the secular rise in bank return on equity. The components of ROE are the operating return ROEA before funding costs, the cost of adjusted debt and deposits (the cost of debt), the leverage spread (ROEA less the cost of debt), and the leverage multiplier (the earning assets not funded by the loan loss reserve and equity divided by the sum of the loan loss reserve and common stockholder’s tangible equity).

Operating Leverage from an Increase in the Operating Return After Tax (ROEA)

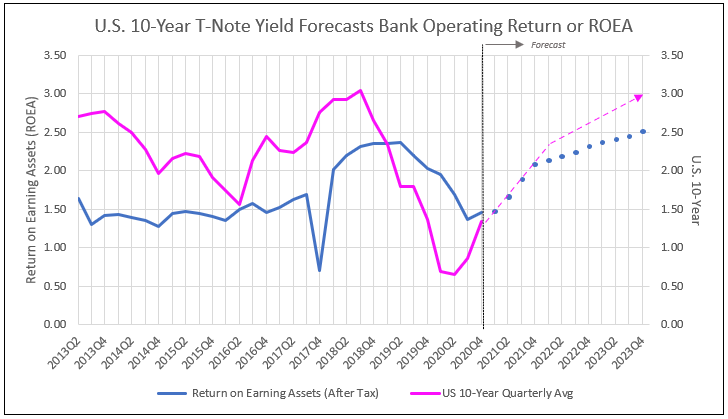

Chart II

ROEA is the operating return after taxes, but before funding cost (see IDC Financial Publishing (IDFCP)’s Methodology below). The ROEA for all bank holding companies was 2.03% as of year-end 2019, declined to a low of 1.37% in the third quarter 2020, and is forecast to recover to 2.15% by March 31, 2022. The ROEA forecast is based on the U.S. 10-year yield increasing to 2.4% by late 2021 (see Chart II). The continued rise in the 10-year to 3% by year-end 2023, raises the forecast of ROEA to 2.50% by December 31, 2023.

Leverage Spread Increases as the Cost of Funding Adjusted Debt Remains Low

Chart III

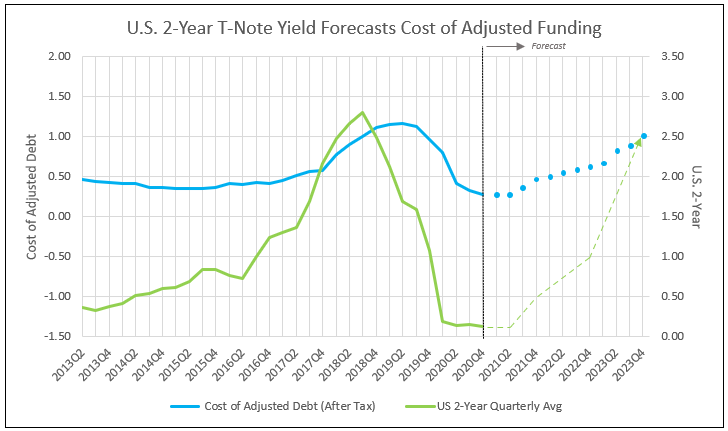

The cost of adjusted debt from funding was 28 basis points as of December 31, 2020 and expected to remain in a range of 30 to 60 basis points until 2023. Controllable inflation forecasts a rise to 50+ basis points, while rapid inflation by 2023 forecasts a recovery to 1%. The 2-year T-Note is used to forecast the bank cost of funding adjusted debt (Chart III). The leverage spread therefore has recovered from 1.16% on December 31, 2020, to 1.6% in 2021, and will rise to 1.7% in 2022.

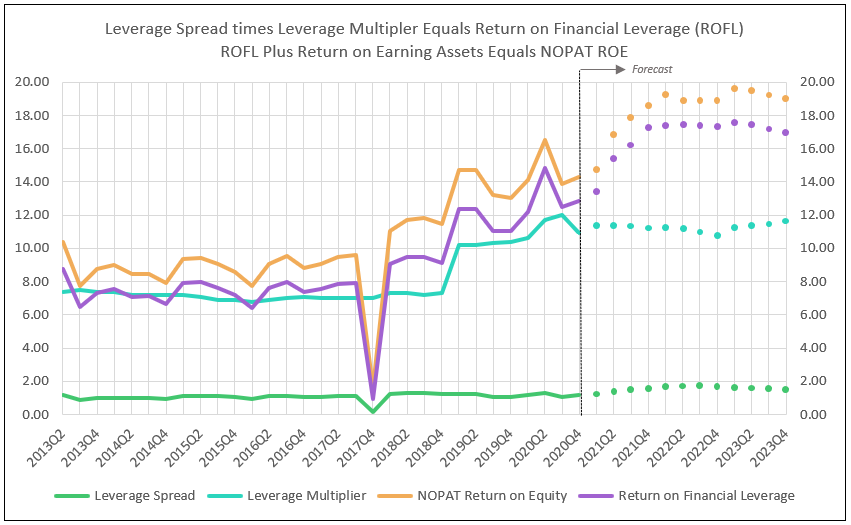

High Financial Leverage Enhances Return on Financial Leverage

Chart IV

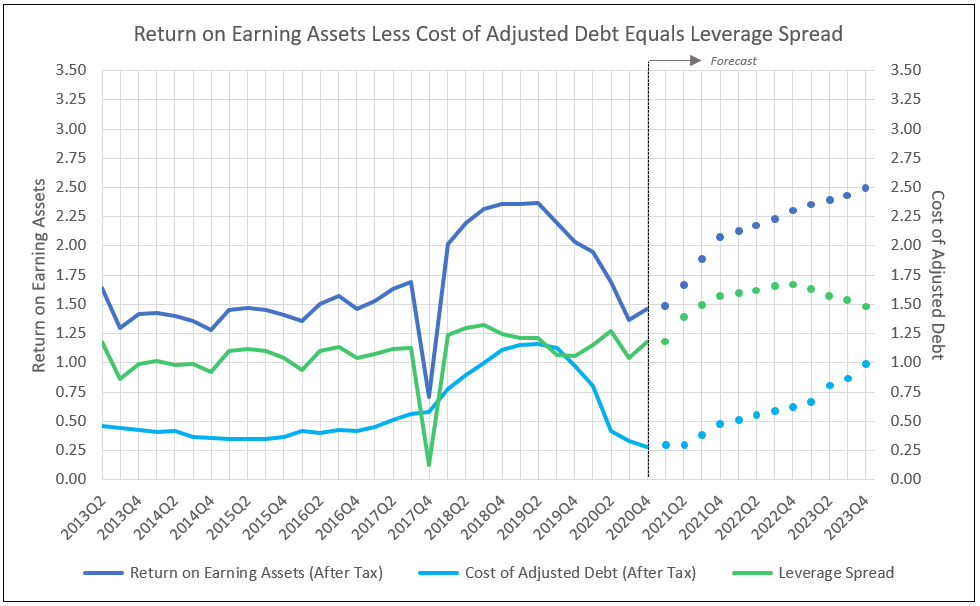

Return on financial leverage (ROFL) is the result of multiplying the rising leverage spread times leverage multiplier. The leverage multiplier, currently a decade-high 10.8, times the leverage spread of 1.2%, provides a ROFL of 13.0%, up from 12.3% at the end of 2020.

As the leverage spread widens from 1.2% to 1.6% by year-end 2021, and to 1.7% by year-end 2022, the leverage multiplier (around 10.5) dramatically increases the return on financial leverage (ROFL). As a result, ROFL is forecast to reach to 17.1% by year-end 2021.

Both Operating and Financial Leverage Benefit the Bank Stocks in 2021, 2022 and 2023 as the NOPAT ROE Increases to Record Highs

Chart V

Adding the operating return (ROEA) to the financial return (ROFL) equals IDCFP’s definition of Net Operating Profit After-Tax Return on Equity (NOPAT ROE). NOPAT ROE rose from under 10% from 2013 to 2016, to 11% in early 2018, to 14% in 2019, and forecast to reach 19.3% by March 2022 (see Chart V).

Leverage from a Higher NOPAT ROE Less COE Drives a Rising Price to Tangible Book Value

Due to the increase in return on equity (NOPAT ROE), the reinvestment rate from bank earnings increases. To control the financial leverage or multiplier, banks are required to increase dividends and stock buybacks. The high reinvestment rate coupled with rising stock buybacks that reduce shares outstanding, accelerate the growth in TBVPS to over 10% a year.

Estimating appreciation potential for a bank stock requires the following to calculate a target price:

- Projection of tangible book value per share (TBVPS) one year into the future.

- Forecast of NOPAT ROE one year ahead.

- Forecast of cost of equity capital (COE) based on the 30-year T-Bond yield one year ahead, with COE adjusted for bank-specific risk.

- The spread between ROE and COE determines the projected price-to-book, which is then multiplied by forecast TBVPS to calculate the target price.

The favorable ROE of over 19% in 2022 and 2023 is offset by a rising COE, due to the increase in the 30-year T-Bond yield. A 3% yield on the 10-year raises the 30-year to 3.8% and increases the cost of equity capital to 6.6%. The spread between NOPAT ROE and COE is 12.4%. In a fully valued bank stock market, like in February 2018 or December 2019, this spread prices a higher multiple of 2.4 times projected TBVPS. Up from a today’s multiple of 1.7, the projected target price for the BKX* of 189 provides a 43% appreciation potential from April 6, 2021 to March 2022 (see Chart I), outperforming the averages of value and epicenter stocks.

Due to these multiple forms of leverage in a recovering economy with rising yields, bank stocks outperform value stocks, as represented by the Russell 1000 value stock index. In past bull markets in bank stocks, IDC Financial Publishing (IDCFP) forecasts proved accurate. For example, the BKX* over 20 months, from 6/30/2016 to 2/22/2018, rose to 103.6% of the target price for February 2018. The price appreciation over 20 months was 97.1% and the forecast for the price appreciation was 92.0%. Our projection on the target price today uses the same process as in past years.

*Large Money Center, Regional and Credit Card Banks

Methodology:

The Traditional ROE Equation and the Problem with the Bank Stock Analysis

The traditional ROE equation simply divides net income by the average of common stockholder’s tangible equity capital. The stockholder ROE, as a bottom-line measure of profitability, fails to reflect the true nature of asset value. In addition, the traditional components of the ROE ratio – net interest margin, net income return on assets (ROA), and resulting stockholder ROE – confuse the source of net income by subtracting cost of funding so early in the analysis. Bank common stock evaluation is unable to separately compare operating and financial returns. Also, accounting for the loan loss provision, and not adjusting net income for the increase on the loan loss reserve, fails to reflect the true cash flow to earnings.

The NOPAT ROE Equation and ROEA, a Measure of Operating Returns

In contrast (IDCFP) uses the NOPAT ROE equation to express ROE as a sum of two components, operating return (ROEA) and financial return (ROFL). ROEA equals the return that the bank earns on loans, securities, cash equivalents and other earning assets, after operating expenses and taxes, but before the loan loss provision and interest expenses on the deposit and debt funds. ROEA focuses on the operating strategy, which identifies returns from investments, loans, and non-interest income sources net of expenses and taxes, plus the increase in the loan loss reserve, all as a percent of earning assets.

Return on Financial Leverage (ROFL), a Measure of Financial Returns

The second component is the bank’s return on financial leverage (ROFL). This reflects both the degree to which the bank uses deposit and debt funds to finance its operating strategy and the cost of these debt funds. A bank’s return on financial leverage (ROFL) measures the efficiency with which the bank uses deposits, borrowings, and other forms of debt to leverage or fund earning assets, not funded by tangible equity capital and the loan loss reserve. ROFL is the product of the bank’s ‘leverage spread” and “leverage multiplier.”

The leverage spread is the difference between the after-tax ROEA and the after-tax cost of funding. The after-tax cost of funding equals interest expenses divided by the net adjusted debt.

Adjusted debt (equal to total earning assets less tangible equity capital and the loan loss reserve) is the remaining amount of earning assets funded by deposits, borrowings, or other debt. The leverage multiplier is the ratio of adjusted debt divided by the sum of tangible equity capital and the loan loss reserve.

The addition of the operating return (ROEA) plus the financial return (ROFL) equals the net operating profit (after tax) return on equity (NOPAT ROE).

For a more detailed graphic of IDCFP’s Common Stockholder Net Operating Profit (After tax) ROE Equation click here.

To view all our products and services please visit our website www.idcfp.com.

For more information about our Deposit Database, or for a copy of this article, please contact us at 800-525-5457 or info@idcfp.com.

John E Rickmeier, CFA, President, jer@idcfp.com

Robin Rickmeier, Marketing Director