Inflation Peaks in Early 2022

Summary of Inflation

The rapid pickup in inflation boils down in large part to the mismatch between supply and demand. With the help of a massive government stimulus, a surge in household purchases strained factories and lengthened global supply chains. Current constraints of U.S. producers trying to ramp up production were made worse by a smaller pool of available labor. The tight labor market, in which the unemployment rate is now 4% (with relatively low participation rates of 62.2% - below the rate in 2019 at 63.3%), has led employers to bid up wages in an attempt to fill millions of job openings and retain workers.

Reasons for Inflation to Peak in 2022

1. “[February’s] NFIB [small business] report was really encouraging. Both wage and pricing intentions have finally rolled over. Firms are stepping up capex plans and curbing hiring intentions. And the inflation stresses from the mini-inventory cycle are in the rear-view mirror.” – David Rosenberg, former Merrill economist, on Twitter

2. Wages are rising due to the shortage of labor as participation rates drop, but in the future post-pandemic economy, eligible workers return to the workforce, including early retirees as inflation drains savings. Also, as sited in the NFIB small business report, wage increases, which have been the highest among the lowest tier of economic earners, are slowing.

3. A peak in the price of crude oil. While the price of crude oil is excluded from Core PCE, higher energy and gas prices directly impact wage gains and input costs. The reasoning for higher prices in oil, gas and electricity is that the oil market feels like a runaway train, speeding toward $100 a barrel or even higher, and in oil, OPEC+ is behind the price hike, adding too few barrels too slowly, allowing inventories to decline to low levels.1

Oil balances are a lot tighter than the International Energy Agency thought, as refineries and petrochemical plants in China and Saudi Arabia report higher thruput or lower crude balances. The group published a recent report, revising historical oil demand back to 2007. The revision, 2.9 billion barrels of additional demand, is huge. Therefore, estimated stockpiles of 660 million barrels of surplus that the IEA saw a month ago have evaporated. The demand revision now estimates global oil stockpiles fell below their year-end 2019 levels.1

Ed Morse, a contrarian, and the long-time head of commodity analysis at Citigroup, Inc,. told clients to sell December 2022 oil contracts at $82.39. “Today everyone seems bullish in the oil market, just like 2008 when Brent crude prices hit a record high of $150 a barrel, only to crash a few months later.”2 Morse agrees today’s oil market is tight and Russia-Ukraine tensions are high, but he anticipates a change in the second half of 2022. In his analysis, the market will shift from tight to surplus in the spring of 2022. The shift is due to rising production from OPEC+, the Permian Basin and other U.S. shale basins, plus Canada and Brazil. To reinforce Morse’s argument, Conoco Phillips announced Permian alone may add 900,000 barrels a day in 2022. An Iran and U.S. agreement could add more oil, and Mideast oil countries in view of $100 oil prices could add to output a total of 3 million barrels. The spring is worth watching for signs of more supply. Note, the Brent December 2022 futures price was $84.72 on February 16, 2022.

4. DeepMacro research uses alternative datasets to gain lead time of key economic indicators. For inflation, they combine consumer prices, producer prices, trader outlook, sentiment expectations and other indicators. In the other category, they point out a collapse in waiting times for truck drivers across the country, indicating supply chain tightness is easing (from Fundstrat research, Feb. 15, 2022). The NY Fed reports a surprise decrease in short and medium-term inflation expectations, i.e., 1-year 5.8% from 6.0%, monthly 3.5% from 7.0%. Market based inflation indicators (implied inflation) over 5-and 10-year spans remain elevated, but off November highs.

A disappointment came from the wholesale price for February, up 1.0 month-to-month and 9.7% over the last year. Wholesale are list prices and as supply increases so do discounts from list prices in coming months.

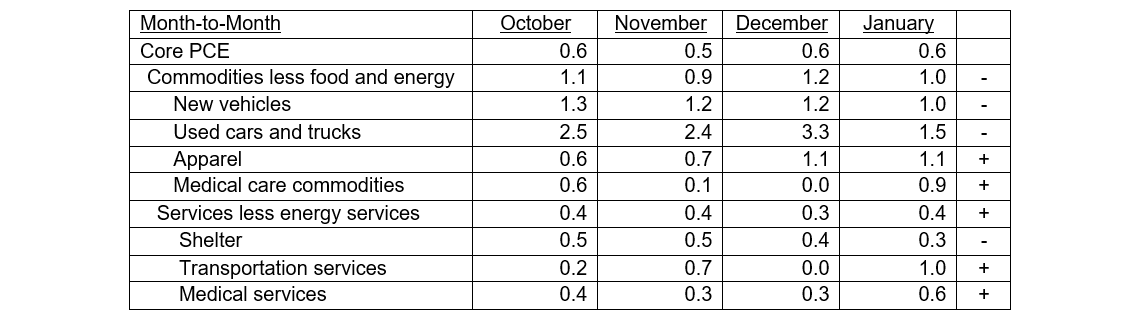

5. The month-to-month changes in Core PCE components, from the CPI report, with the largest percentage change in October, November, and December, slowed in January 2022 (see minus signs in Table I).

Table I

Percent Change in CPI for All Urban Consumers

The Federal Reserve is basically of the view that the current inflation is too high, but related to the pandemic, which should normalize over time. Core PCE and sticky CPI should recede to 2.5% to 3.0% by late 2022 or in 2023.

Housing Continues to Be Strong Driver of Inflation

Rent and owners’ equivalent rent (OER)—the amount of rent equivalent to the cost of ownership—are among the most important components of the Consumer Price Index (CPI) and the personal consumption expenditures (PCE) price index.3

The Dallas Fed forecasting model shows that rent inflation and OER inflation are expected to increase materially in 2022 and 2023. Given their weights in the core PCE price index, rent and OER together are expected to contribute about 0.6 percentage points to 12-month core PCE inflation for 2022 and about 1.2 percentage points for 2023.3

These forecasts also suggest that rising inflation for rent and OER could maintain the overall and core PCI and PCE inflation rates above 2 percent in 2023, when current supply bottlenecks and labor shortages may have subsided.3

Conclusion

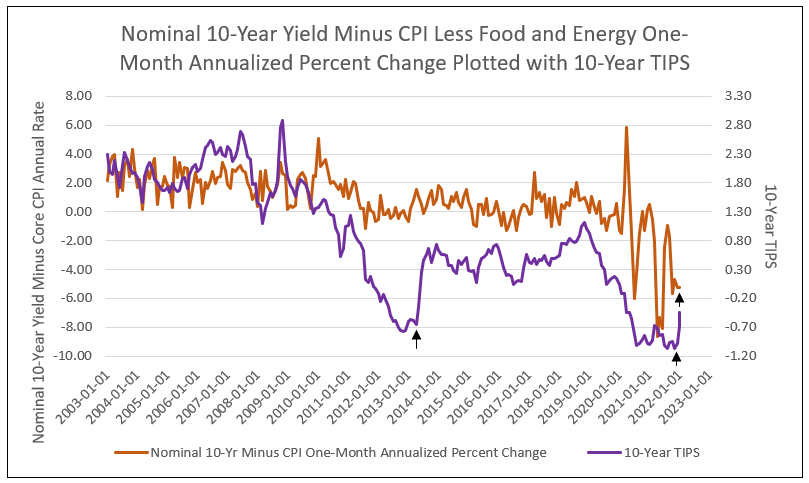

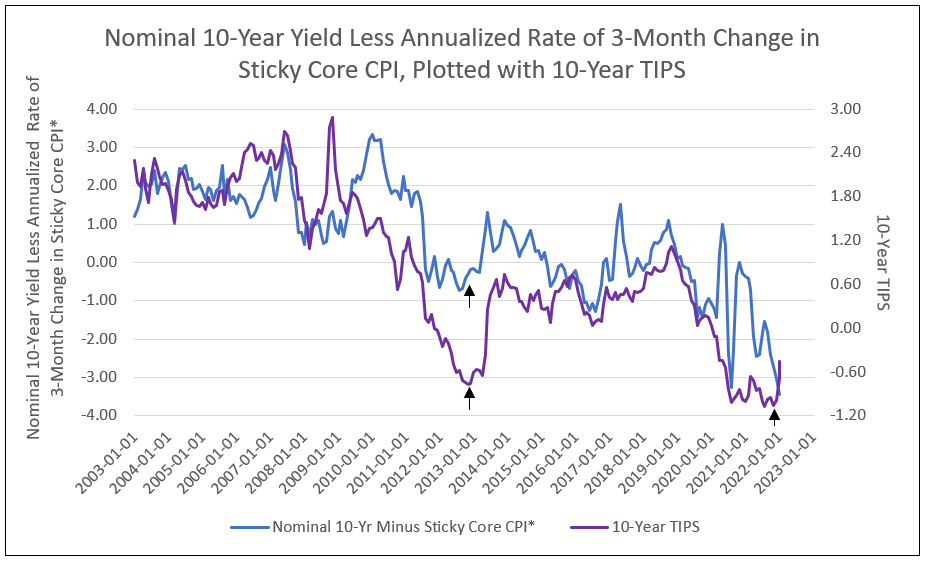

The following charts illustrate how rising TIPs yields forecast lows in the nominal 10-year yield minus inflation.

Chart I

Chart II

*Sticky Price Consumer Price Index Less Food and Energy, Monthly, 3-Month Annualized Percent Change, Seasonally Adjusted. The Sticky Price Consumer Price Index (CPI) is calculated from a subset of goods and services included in the CPI that change price relatively infrequently. Because these goods and services change price relatively infrequently, they are thought to incorporate expectations about future inflation to a greater degree than prices that change on a more frequent basis. Source: St. Louis Fed

We conclude the Federal Reserve opinion that the current rise in inflation is too high, but will recede by 2023, is correct.

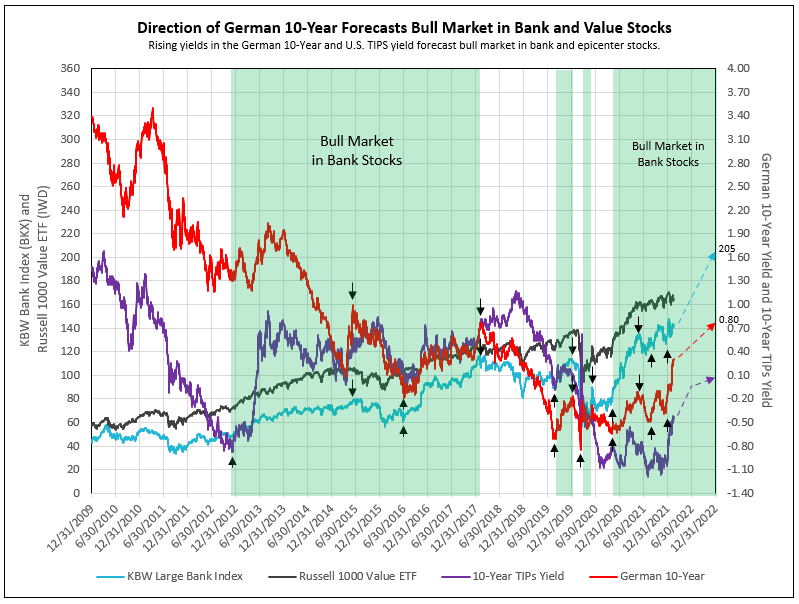

Bull Markets in Bank Stocks

- Since 2015, the bull markets in bank stocks began with a cycle low in the German 10-year confirming a low in the U.S. 10-year yield (see Chart III).

- The first leg of bull market in bank stocks began in October 2020 and ended in mid-May 2021, as the German 10-year yield reached its peak of -0.11%.

- An intermission occurred between legs from May to July/August 2021, as the German 10-year yield declined to its cycle low.

- The next upward leg of the bank bull market began in July 2021 followed by the German 10-year recovering to a positive 0.3% yield and the BKX (large bank stock index) about to increase to new cycle highs.

- With the TIPs yield at -0.45% and headed to zero, the nominal 10-year rises to 2.4% to 3.0% in 2022, steepening the yield curve. Banks stocks (BKX) offer a 46% appreciation potential.

Chart III

1 OPEC+ Must Fix Its Million-Barrel Supply Gap, IEA Says

2 What If Goldman Is Wrong and a Lonely Oil Bear Is Right?

3 Surging House Prices Expected to Propel Rent Increases, Push Up Inflation

To view all our products and services please visit our website www.idcfp.com. For more information about our ranks, or for a copy of this article, please contact us at 800-525-5457 or info@idcfp.com.

John E Rickmeier, CFA

President

jer@idcfp.com

Robin Rickmeier

Marketing Director