The Bond Market is King with HYG Calling the Low in the S&P 500

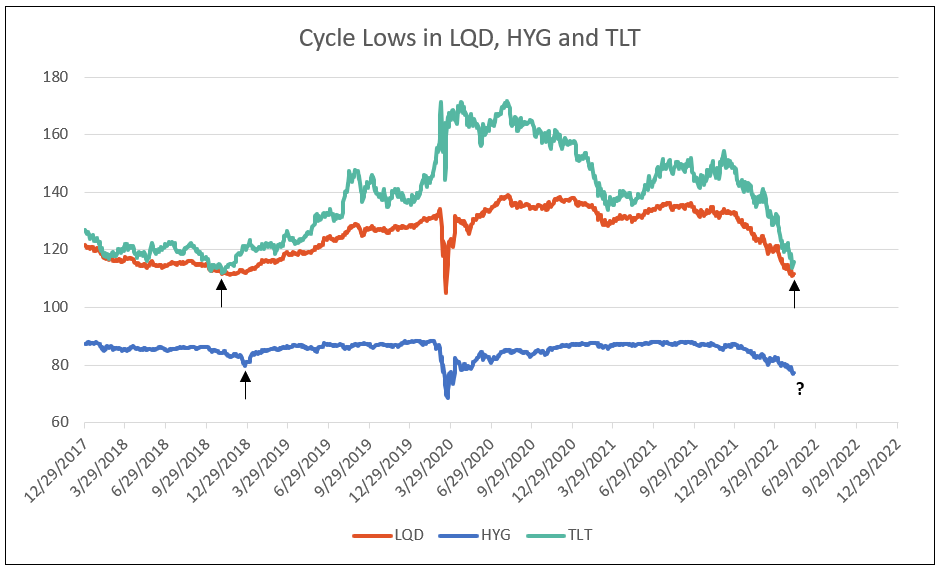

Cycle lows in the High Yield Bond ETF (HYG) historically have occurred at the lows in the stock market (see Chart I). U.S. 10-year yield and high yield bonds have priced in inflation peak and future Fed funds rate increases.

The technical picture from DeMark provides a 13 sequential sell signal on the 10-year yield (TNX), a buy setup of nearing 13 on the price of the 20+ year Treasury Bond ETF (TLT), a weekly 13 buy on investment grade bond ETF (LQD), and a 9 buy setup for the High Yield Corp Bond ETF (HYG, a bond market proxy for equities) following a series of daily 13 buy signals in March and early April (a potential major low). Confirmation of buy comes from the Chaikin Money Flow reaching an extreme low (see Charts I and II).

High Yield Bond ETF (HYG) Forecast to Reach a Low in May/June of 2022

Chart I

Major Bond ETFs Reach a Cycle Low

The prices of the 20+ year Treasury Bond ETF (TLT) and the Investment Grade Corporate Bond ETF (LQD) reached cycle lows on May 10, nearly equal to the cycle lows on October 29, 2018. On December 17, 2018, there was also a cycle low of the High Yield Bond ETF (HYG). (See Chart II).

Given the technicals indicating a price low in these ETFs, a cycle low in the HYG is expected in May/June 2022. In anticipation of the coming low, bank stocks have started to bottom and perform.

Chart II

Inflation Peaks in the Second Quarter of 2022

One-month core PCE, the Fed’s gauge on inflation, is expected to peak at the reported 0.6% in April, equal to December and January highs and decline to 0.3% by June. The year-over-year increase is forecast to fall to 3.6% by year-end 2022 and 2.4% by the end of 2023. After two 50 basis point increases in the Fed funds rate, Powell indicates further increases might slow.

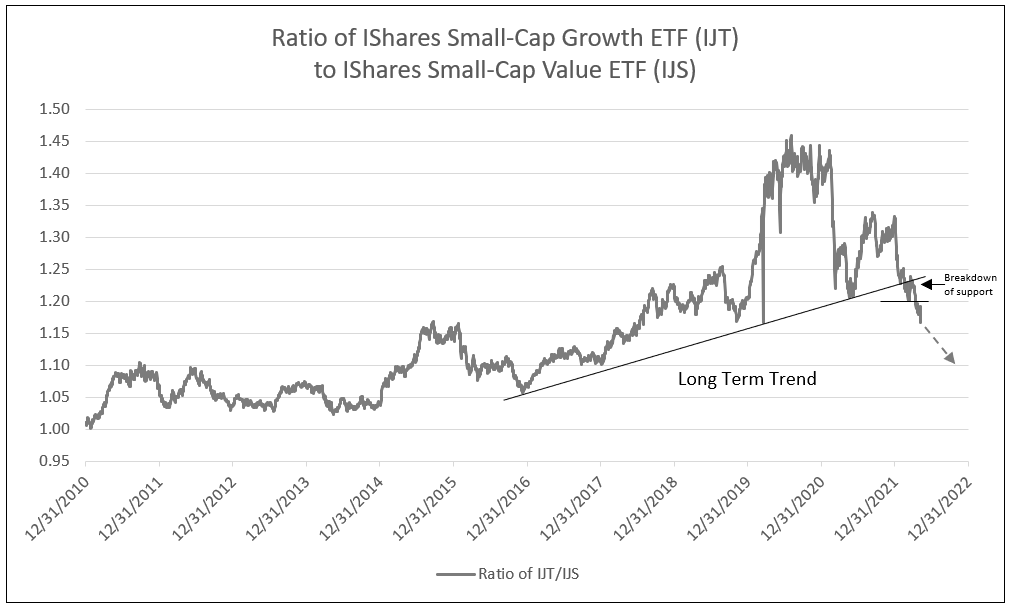

Structural Change in the Stock Market Favoring Value Stocks

In October 2020 and again in late 2021, the peak and significant decline in Small-Cap Growth ETF (IJT) relative to Small-Cap Value ETF (IJS) illustrated the structural change in the stock market. A decline below both the trend line from 2016 to 2021 and the cycle low in early 2021 indicated a trend favoring value stocks (see Chart III).

Small-Cap Growth Continues to Break Trends and Underperform Value

Chart III

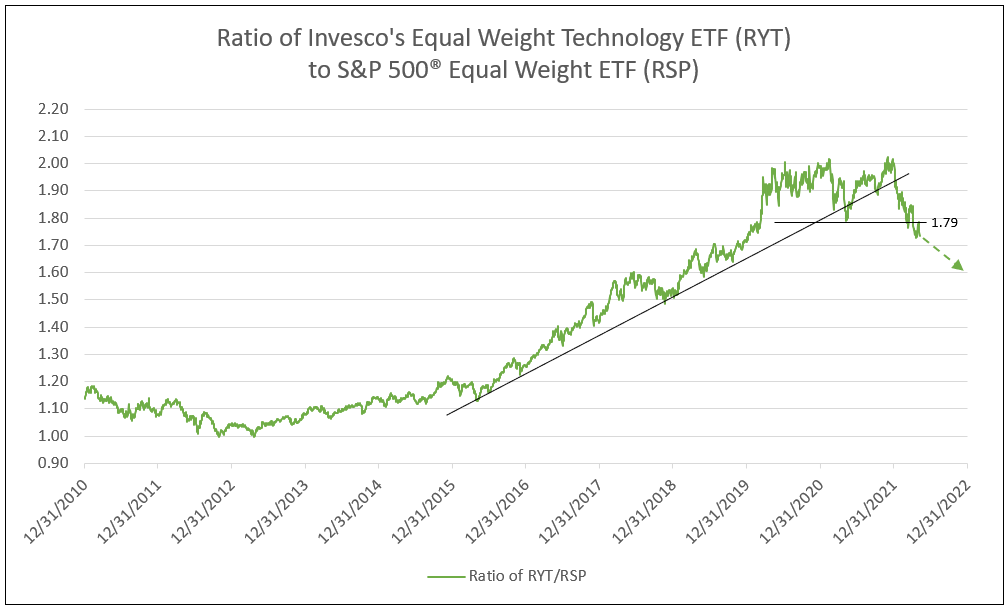

Following the peak in late 2021, Equal Weight Technology ETF (RYT) fell relative to Equal Weight S&P 500 ETF (RSP), declining below the low in early 2021, and indicating a trend favoring value stocks (see Chart IV).

In an Environment of Higher Yields Equal Weight Technology Underperforms Value

Chart IV

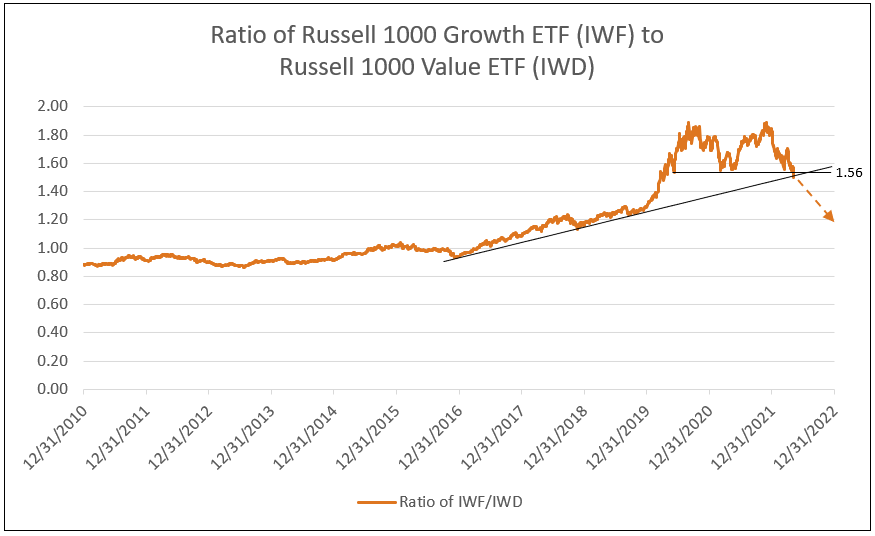

The decision point between the Large Cap Russell 1000 Growth ETF (IWF) compared to the Value ETF (IWD) has arrived. The trend lines from 2016 and the lows from 2017 converge at 1.56, which is the ratio of IWF to IWD. In April the ratio declined below 1.56 to 1.55, indicating a major structural change in large cap stocks, favoring value (see Chart V). A further decline in the ratio of IWF/IWD to 1.20 is forecast later in 2022, given the strong economy for the second half of the year and the superior performance of bank stocks.

Decision Point: A Decline Below 1.56 in 2022 Indicates Major Institutions Favor Value Over Growth Stocks

Chart V

The Russell 1000 Value ETF dramatically outperformed FANG+ stocks, reaching new cycle highs since the fourth quarter of 2021. Following a correction in March 2022, the ratio of IWD to FNGS continues to recover, reaching new highs as value stocks outperform (see Chart VI).

The Ratio of Russell 1000 Value ETF to FANG+ Stocks Reaches New High in May 2022

Chart VI

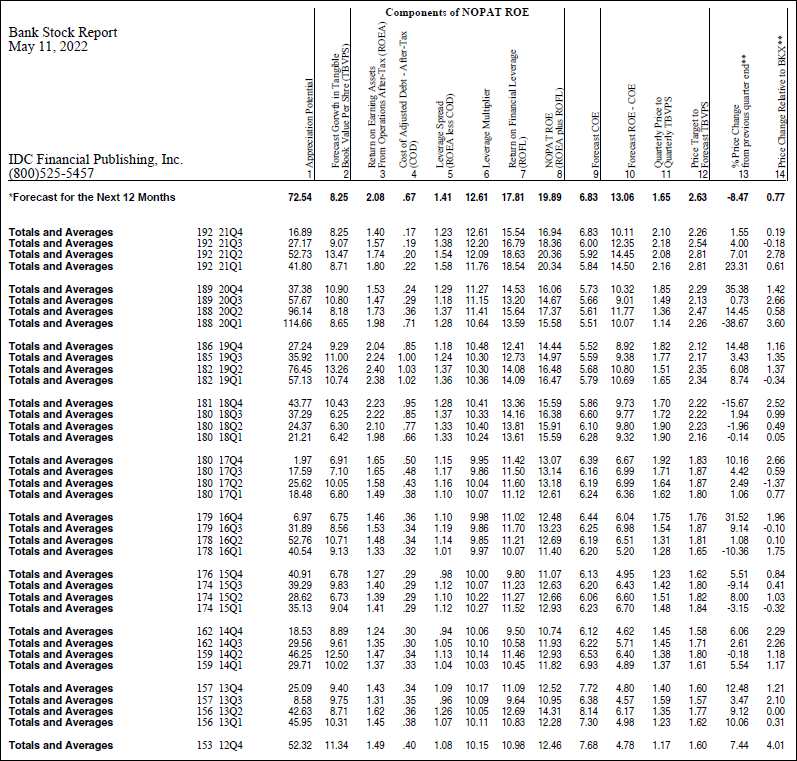

Bank stocks continue to build fundamentals for accelerating EPS growth, as return on equity is forecast to increase over the 21% mark in 2022 and 2023. In the current environment of a dramatic rise in the Fed funds rate to 2.5% in 2022 or early 2023, with an associated reduction in the Fed’s balance sheet, bank operating returns (ROEA) rise faster than the cost of financing (COD). Combined with increasing leverage, the result is a continued secular rise in ROE to new highs and, therefore, growth in TBVPS and accelerating EPS growth (see Table I).

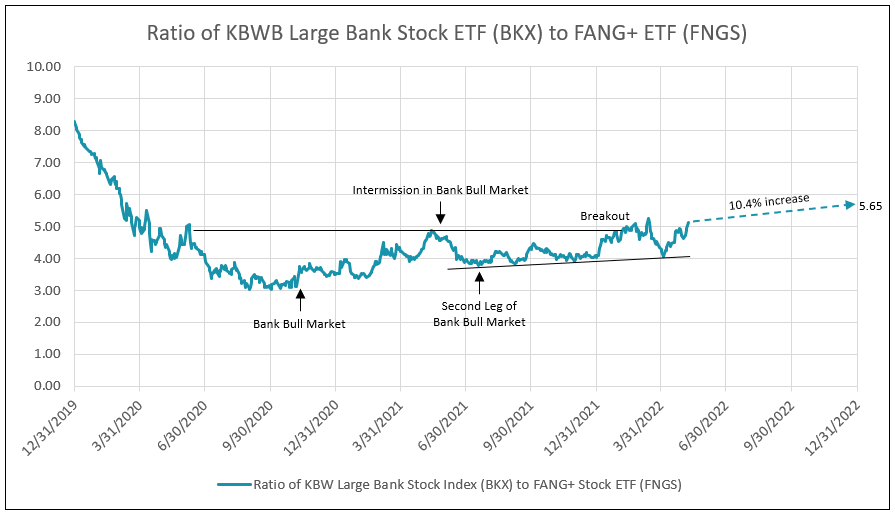

Impact from the war in Ukraine, higher inflation in the non-core categories food and energy, and potential recession fears, depress bank stocks relative to the Russell 1000 Value ETF (see Chart VII). A realization that inflation has peaked, witnessing a declining impact from the conflict between Russia and Ukraine, and the outlook for continued economic expansion, together, propels bank stocks relative to other value stocks (and especially FANG+ growth stocks) in the coming months.

Bank Stocks Recover in May 2022

Chart VII

The bank forecast for 19.9% Roe and 6.8% COE provides a forecast ROE less COE of 13.1%, which in turn projects a forecast target price-to-forecast TBVPS of 2.6. Given an 8.3% forecast increase in TBVPS and a 59.4% change from the current price to TBVPS (Table I, Column 11) to the price target to forecast TBVPS (Table I, Column 12), there is a forecast of 72.5% in potential price appreciation.

Table I

Let IDC provide you the value and financial history of your favorite bank stock. For you to better understand our process of valuation, we offer a free, one-time analysis of one of the 202 banks in our bank analysis database. Simply send your request with the bank stock symbol to info@idcfp.com.

To inquire about IDC’s valuation products and services, please contact jer@idcfp.com or info@idcfp.com or call 262-844-8357.

John E Rickmeier, CFA

President

Robin Rickmeier

Marketing Director