Inflation Nowcasting Captures Slowdown in Inflationary Drivers

Forecasts for July CPI

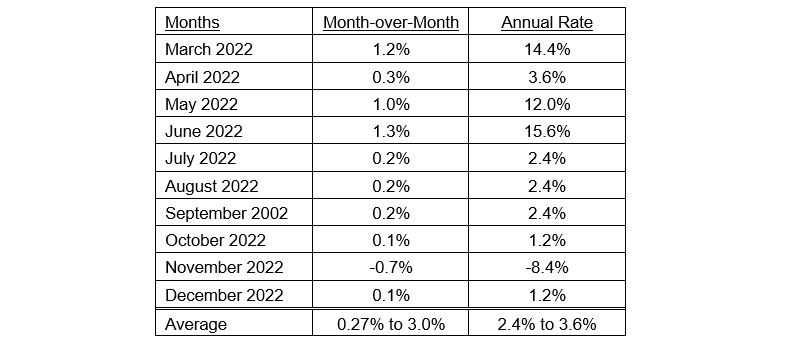

Forecasts of the slowdown in July CPI, released on August 2, were captured in the Inflation Nowcasting from the Cleveland Federal Reserve. The July month-to-month CPI is estimated at 0.27%, followed by less than 2% monthly increases to December 2022, as indicated by the swap market.1

The Cleveland Fed Inflation Nowcasting shows July CPI indicating 0.27%. This is a 3.24% inflation rate annualized versus a recent reported year-over-year CPI inflation rate of 9% to 12%.

Table I

Monthly Inflation Nowcasting, Federal Reserve Bank of Cleveland

Lowest since January 2021

Inflation Swap Markets Forecast Less Than 2% Annualized Inflation for the Next Six Months

The second half of 2022 is set to experience multiple drivers forecasting declining inflation, including lower gasoline prices, excess inventory liquidation, a drop in food prices reflecting lower commodity prices and weak travel data, all captured by the swap market.1

Table II

CPI Per Swap Market

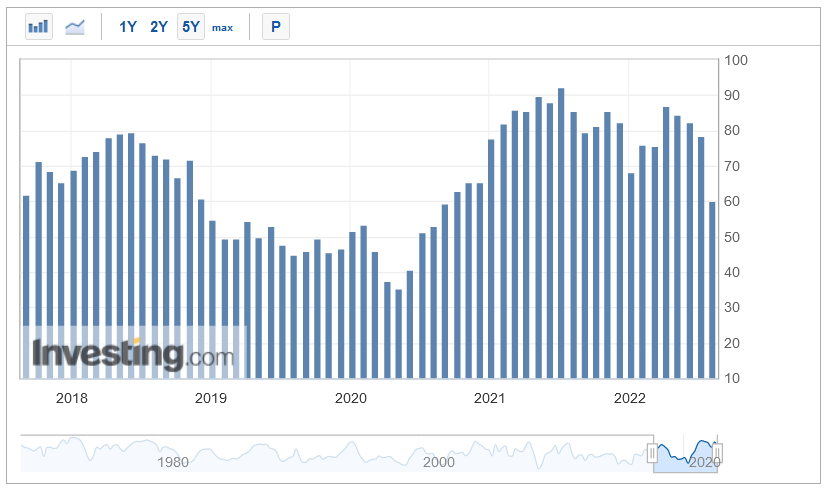

U.S, ISM Manufacturing Prices Paid Index Declines from 79 in June to 60 in July

The Institute of Supply Management (ISM) Manufacturing Purchasing Managers Index (PMI) Report on Business is based on data compiled from monthly replies to questions asked of purchasing and supply executives in over 400 industrial companies.2 It indicates a significant drop in expected prices last month to an index of 60, levels not seen since 2019 and early 2020 (see Chart I).

Chart I

U.S. ISM Manufacturing Prices2

Employer Surveys Forecast Slowdown in Wage Growth3

The average for the Business Survey of Wage Expectation peaked at 5% in 2021 and fell to 4.25% at mid-year 2022, indicating wage growth slows to 4.5% by year-end 2022, to under 4% by year-end 2023, and, finally, settling at 3.5% (which is compatible with the Fed 2% target) in 2024.

To support the wage slowdown forecast, Indeed Labs Data1 indicate the following.

- The number of job openings (JOLTS) in July 2022 is below July 2021.

- The first year-over-year decline in job openings was in December 2019.

Given the decline in job openings year-over-year, the conclusion is that the labor market will not support strong wage growth.

The Error in GDP Accounting

According to Jeremy Siegel, Professor of Finance at Wharton, given the last six months added 2.7 million jobs, and another 528 thousand jobs were added in July, reported GDP should not have declined. “What are people doing? You get GDP by people working,” Yet, hours worked held up at previous levels, therefore, a dramatic collapse in productivity, potentially the worst in history, could then be to blame. A snap back in productivity would severely reduce unit labor costs or future inflation.4 Or the GDP accounts are in error with major revisions in the future, potentially indicating better GDP growth in the first half of the year.3

Conclusions

- Month-to-month inflation declines to less than 2% annual rate in the second half of 2022.

- Employment and wage growth continues with wages increasing 4.5%.

- Real wage growth emerges supporting a soft landing and a growing real economy.

- Wage growth slows in 2023, but exceeds CPI change, providing real wage growth. Productivity recovers and unit labor costs decline, reducing core inflation.

Bank Stock Leads Stock Market in Recovery Stage

Bank stocks declined significantly in June as the market priced in recession. Conversely, a soft landing, growth scare, or mild recession priced in these bank stocks set the stage for banks leading the recovery. Since June 30, 2022, regional banks ETF (KRE) is up 10.2%, large banks ETF (KBWB) rose 7.8%, while value stocks ETF increased 5.4%, QQQ advanced 14.8%, and S&P 500 ETF rose 9.6%.

Wall Street’s Top Strategists Saying U.S. Stocks Will Rally in the Second Half Supporting a Bull Market in Bank Stocks

Kolanovic, voted the No. 1 equity-linked strategist in last year’s Institutional Investor survey, has stuck to his calls for risky assets this year despite the sharp rout in the first half. He expects a rebound in stocks on attractive valuations and as the peak in investor bearishness has likely passed.5

“Although the activity outlook remains challenging, we believe that the risk-reward for equities is looking more attractive as we move through the second half,” Kolanovic wrote in a note dated Aug. 1. “The phase of bad data being interpreted as good is gaining traction, while the call of peak Federal Reserve hawkishness, peak yields and peak inflation is playing out.”5

His view that much of the bad news from weak economic data is now priced in and that stocks will end the year “meaningfully higher” is in sharp contrast to calls by counterparts at banks including Goldman Sachs Group Inc., Morgan Stanley and Bank of America Corp.5

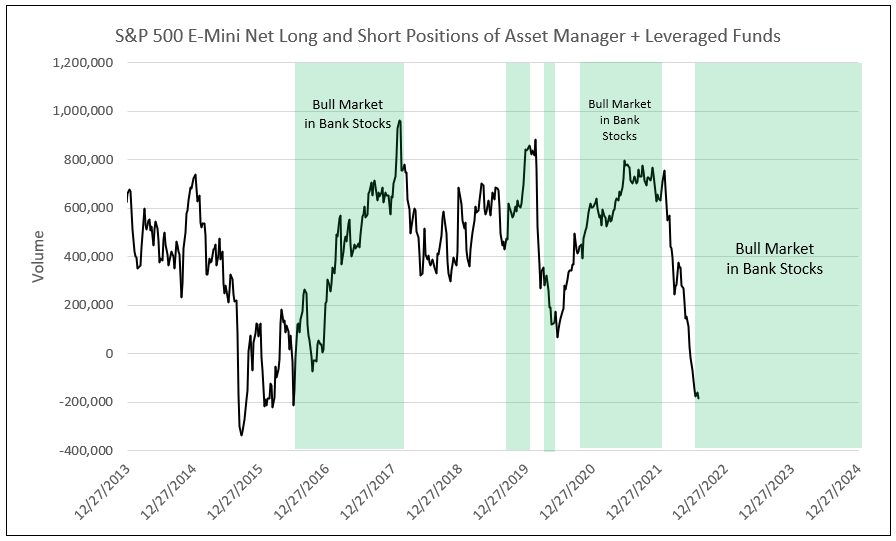

Futures positioning is the most bearish since June 2016 at almost a negative 200k in volume. CFTC S&P 500 E-mini futures net position asset managers plus leverage funds reached a low of a negative 200k in volume on June 30, 2016, and subsequently rose to a peak of 1 million by February 2018 (see Chart II). The rise from the most negative point to the maximum long reading coincided with the major bank stock bull market (BKX), which rose from 60.27 on June 27, 2016, to 116.52 on February 1, 2018, a 93% gain.

The current appreciation potential of the BKX, based on IDC Financial Publishing’s valuation of bank stock components, is 87%.

Chart II

Source: CFTC & Bloomberg

1 - Reported by FSInsight, a Fundstrat company, August 1, 2022

2 - U.S. ISM Manufacturing Prices

3 - Goldman Sachs Research, July 28, 2022

4 - CNBC interview, August 1, 2022

5 - JPMorgan’s Kolanovic Stands Apart in Saying Stocks Will Rebound, Bloomberg

Let IDC provide you the value and financial history of your favorite bank stock. For you to better understand our process of valuation, we offer a free, one-time analysis of one of the 202 banks in our bank analysis database. Simply send your request with the bank stock symbol to info@idcfp.com.

To inquire about IDC’s valuation products and services, please contact jer@idcfp.com or info@idcfp.com or call 262-844-8357.

John E Rickmeier, CFA

President

jer@idcfp.com

Robin Rickmeier

Marketing Director