New Capital Adequacy Standards for Credit Unions

Credit unions with total assets of $50 million and above must now follow different expectations and frameworks when calculating capital ratios. The new capital adequacy standards were implemented on January 1, 2022, from the National Credit Union Administration (NCUA). First issued in October 2015 as a result of the 2009 recession, the standards went through several amendments and implementation delays before taking effect at the start of this year.1

After such a long process to develop and implement the new rule, credit unions impacted by the change may not be aware it is now in effect. These are some frequently asked questions about the new capital adequacy standards and the ratios, limits and details involved.1

What are Capital Adequacy Standards?1

Under the previous rules, effective through December 31, 2021, the Net Worth Ratio (NWR) calculation was required for all credit unions, and the calculation of the Risk-Based Net Worth (RBNW) ratio for all credit unions with total assets greater than $50 million.

RBNW is a lagging ratio, and it does not factor in an asset’s risk level, while the NWR is the primary measure of a credit union’s financial strength. The NWR is calculated by taking the total net worth, as defined for a credit union, divided by total assets.

Why did the NCUA Change the Standards?1

First, the NCUA wanted to address weaknesses observed during the 2007-08 financial crisis. Second, the NCUA wanted to bring capital adequacy standards in line with those of other banking agencies, which amended their capital rules in 2013. Above all else, the NCUA wanted to strengthen capital requirements and improve risk sensitivity.

What Changed Under the New Rule?1

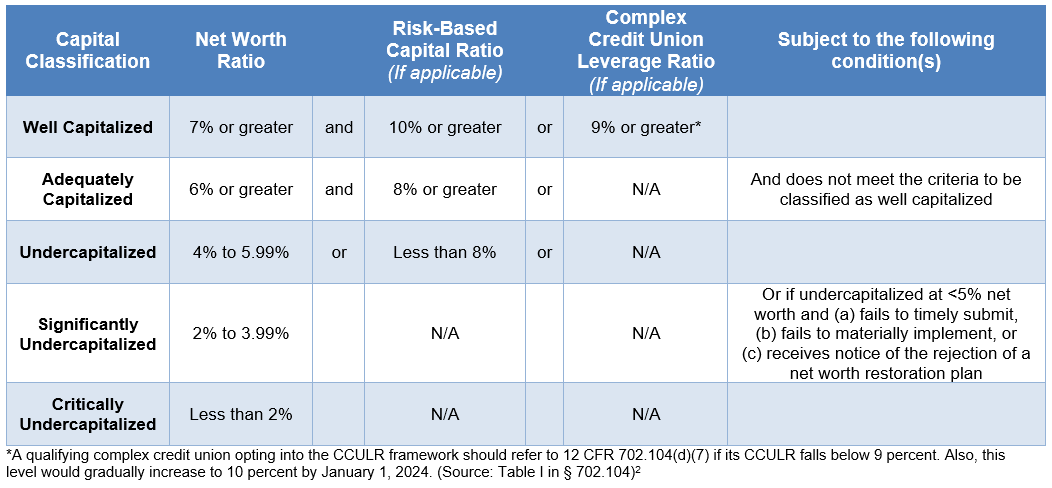

The definition of a complex credit union changed from more than $50 million in total assets to quarter-end total assets of more than $500 million on its most recent Call Report. While all credit unions still must calculate NWR, only complex credit unions must also perform a second capital calculation, following the Risk-Based Capital (RBC) framework or the Complex Credit Union Leverage Ratio (CCULR) framework, if so elected and qualified. For a credit union under $500 million in assets, the net worth in Table I determines their different capital classification, and whether it is well-capitalized, etc.

Table I

Capital Categories

What is the Risk-Based Capital Ratio?1

The ratio is a complex calculation of a credit union’s capital. The ratio increases favorably as the capital elements in the numerator increase but decreases as the risk weighted assets in the denominator increase.

Different assets are assigned a specific risk weight. For example, cash is assigned a zero percent risk weight, while mortgage servicing assets are considered higher risk and, therefore, assigned a risk weight of 250 percent. Risk weighting in this way supports the consideration of capital requirements in asset allocation choices before potential losses and declining capital.

What is the CCULR?1

CCULR is modeled after the Community Bank Leverage Ratio (CBLR). The CCULR dictates that credit unions should hold capital equal to the risks on their balance sheets. This risk-based capital helps to minimize the losses when a financial institution fails. The intent is to simplify requirements for eligible complex credit unions, as it eliminates the requirement to calculate the RBC ratio. The trade-off for this simplicity is that the complex credit union would be required to maintain a higher Net Worth Ratio than if they had elected to use the Risk-Based Capital ratio.

Institutions can opt in and opt out of CCULR during any quarter. If a credit union opts in to CCULR and fails to meet the required thresholds, there is a two-quarter grace period to meet the opt-in requirements, which are:

- Be a complex credit union (greater than $500 million total assets)

- NWR of 9% or more

- Off-balance sheet exposures totaling less than 25% of total assets

- Trading assets and liabilities that comprise less than 5% of total assets

- Goodwill and intangible assets that are less than 2% of total assets

Summary: What’s the Bottom-Line Impact on Credit Unions?1

Credit unions with total assets between $50 million and $500 million no longer need to calculate an RBNW ratio. Complex credit unions with total assets greater than $500 million will no longer calculate the RBNW ratio; instead, they will follow the RBC framework, or, if eligible and so choose, the CCULR framework.

All credit unions will continue to calculate their NWR, which will impact the calculation of MBL limits. Credit unions should review how they calculate their MBL limit to ensure they align with expectations of the National Credit Union Administration.

Comparing Capital Requirements of Credit Unions to Banks

Credit unions have the same percent requirement of a community bank for a well-capitalized rating. Credit unions given a classification of well capitalized with assets less than $500 million are required to have a net worth to total assets ratio of 7% or greater (see Table I). Since the net worth ratio is similar to that reported prior to 2022, the ratio provides continuity over time.

The main difference between banks and credit unions is the net worth used in the credit union ratio to assets includes undivided earnings, other reserves, and subordinated debt included in net worth, but excludes accumulated unrealized net gain (loss) on available for-sale debt securities or cash flow hedges. Bank Tier I equity includes marking-to-market the net gain (loss) on available for-sale debt securities and cash flow hedges, as well as excludes goodwill and other intangibles.

Credit unions with a net worth ratio of 9% or greater, electing the complex credit union leverage ratio and having assets over $500 million are classified as well capitalized. Alternatively, a net worth ratio of 7% or greater and a risk-based capital ratio of 10% or greater in those credit unions that do not elect the complex status are also classified as well capitalized. For credit unions with assets less than $500 million in assets, a net worth ratio of 7% or greater is classified as well capitalized (see Table I).

For large well-capitalized banks, the ratio of Tier I capital to Tier I asset requirement is 5% or greater. In addition, banks are required to have a Tier II capital to risk-based assets ratio of 10% or greater, and a Tier I equity capital ratio of 6.5% or greater. For community banks with less than $10 billion in assets, a 9% Tier I capital ratio is required and risk-based assets are not calculated.

Starting on January 1, 2022, a qualifying community banking organization must have a leverage ratio of 8% or more to qualify for the two-quarter grace period. At the end of the grace period, the banking organization must meet all the qualifying criteria to remain in the community bank leverage ratio framework, including less than $10 billion in total consolidated assets and a leverage ratio requirement of 9% or greater.

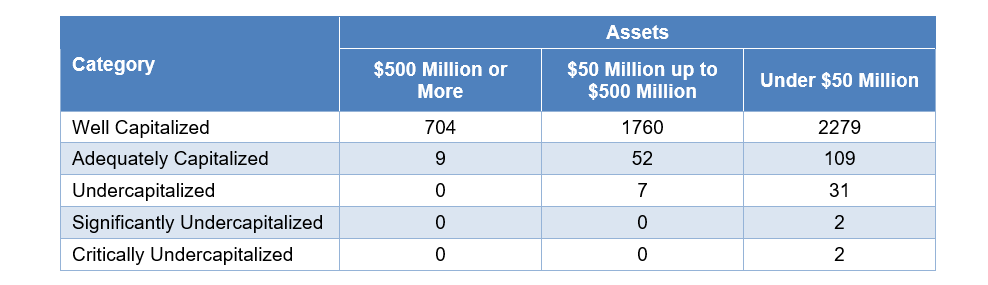

The vast majority of very large credit unions over $500 million, those between $50 to $499 million and those under $50 million in assets are well capitalized (see Table II).

Table II

Credit Unions by Capital Category and Size

Table III

1 NCUA 2022 Capital Adequacy Standards: Find Out if Your Credit Union is Affected by the New Rule RKL

2 Code of Federal Regulations § 702.104

To view all our products and services please visit our website www.idcfp.com. For more information, or for a copy of this article, please contact us at 800-525-5457 or info@idcfp.com.

John E Rickmeier, CFA

President

jer@idcfp.com

Robin Rickmeier

Marketing Director