Inflation is a Monetary Phenomenon

Milton Friedman famously said: “Inflation is always and everywhere a monetary phenomenon, in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.”

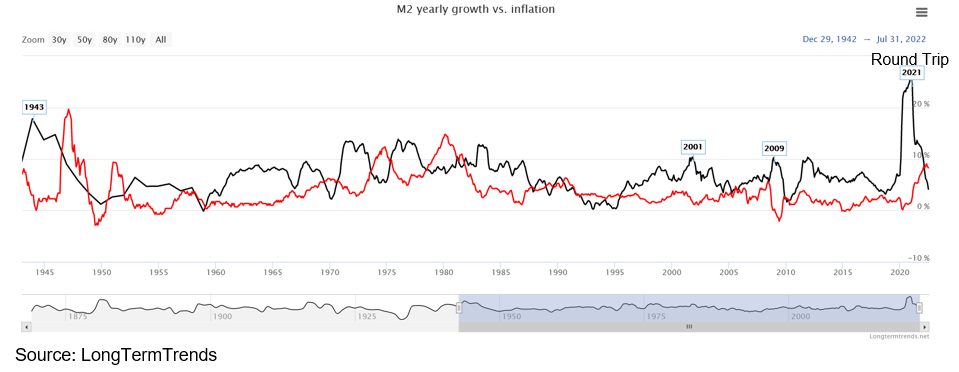

M2 money supply growth has accelerated from 1.9% in the fourth quarter of 2018 to 25.0% in the fourth quarter of 2020, the highest in 150 years. In the second quarter of 2020, inflation reached a low, but the Fed failed to raise the Fed funds rate to control accelerating inflation in 2021 and 2022 until March of this year.

Following its peak at 25.0%, M2 money supply made a round trip and fell to 4.1% in the third quarter of 2022. Based on its 24-month lead time, CPI inflation is expected to peak in the fourth quarter of 2022 and recede to under 3% by the end of 2023 (see Chart I). Given this outlook, why would the Fed continue to raise the Fed Funds rate above 4% later this year and in early 2023? Is the Fed about to make another mistake?

Chart I

M2 Money Supply Growth Vs Inflation

Warning from Jeremy Siegel

According to Jeremy Siegel, Professor of Finance at the Wharton School of Business, if the Fed waits for CPI core inflation to hit 2%, the Fed will drive the economy into depression. Later in this article, we discuss the sticky component of rent. Lagged shelter components of owners’ equivalent rent (OER) and rent of primary residence were up 0.7% and 0.8% respectively in September, but should have been -0.7% using current housing and rent data. Dr Siegel called the reported Fed shelter increase, which is 32.5% of CPI and 41.6% of core CPI, absolutely ridiculous as a measurement of inflation (see Charts IV, V and VI).

Dr Siegel further indicated that the Fed should focus on 1) money supply growth, 2) financial and liquidity indicators on both bonds and stock markets, and 3) commodity prices. The Fed should increase the funds rate by another 50 basis points in November 2022, then pause to let these three inflation indicators guide further Fed actions.

Two Sectors Account for Almost all of the Increase in CPI1

Shelter inflation represented 0.25% of the 0.39% September CPI increase, or 64% of the gain. Auto-related components represented 4 of the top 10 categories (leased cars, insurance, new cars, and car repair) totaling 0.14% of the 0.39 CPI increase or 36% of the gain. The Fed is relying on the 17-month lagging shelter inflation measure and auto availability due to supply restraints to determine the future Fed funds rate.

UIG Measures and 12-Month Change in CPI2

- The Underlying Inflation Gauge (UIG) “full data set” measure from the New York Federal Reserve for September is currently estimated at a 4.4% year-over-year increase, a 0.1 percentage point decrease from the previous month.

- The “prices-only” measure for September is currently estimated at 6.0%, unchanged from the previous month.

- The 12-month change in the September CPI was +8.2%, a 0.1 percentage point decrease from the previous month.

Chart II

Underlying Inflation Decelerates Toward 3%

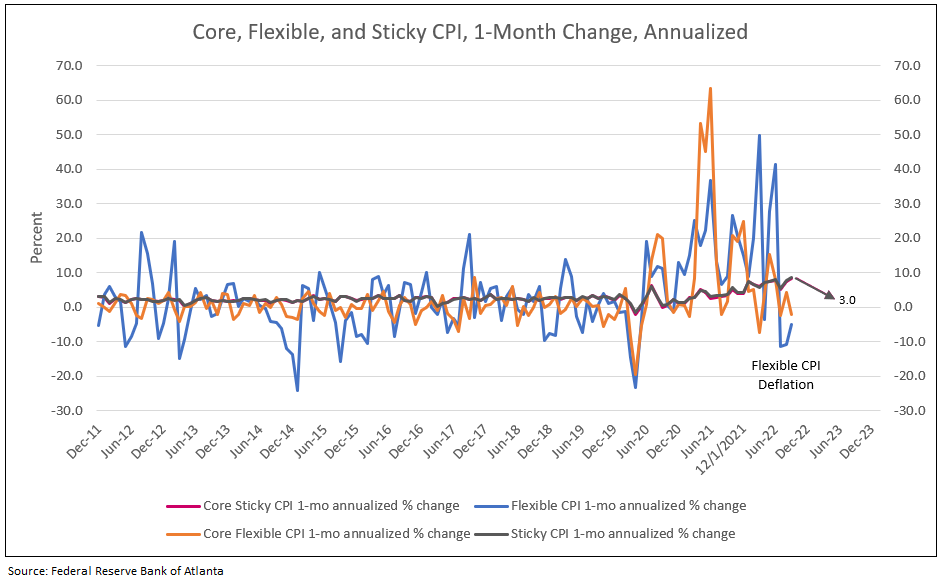

Core, Flexible and Sticky Prices

The percent change in flexible one-month price remained at a negative 6%, while core sticky price (due to services mentioned above) remained high but expected to decline to 3% by 2023 (see Chart III and Forecast of Rent below).

Chart III

One-Month Change in Flexible CPI Peaked in the Summer of 2021 and Fell to Negative Levels in August and September at Annual Rate

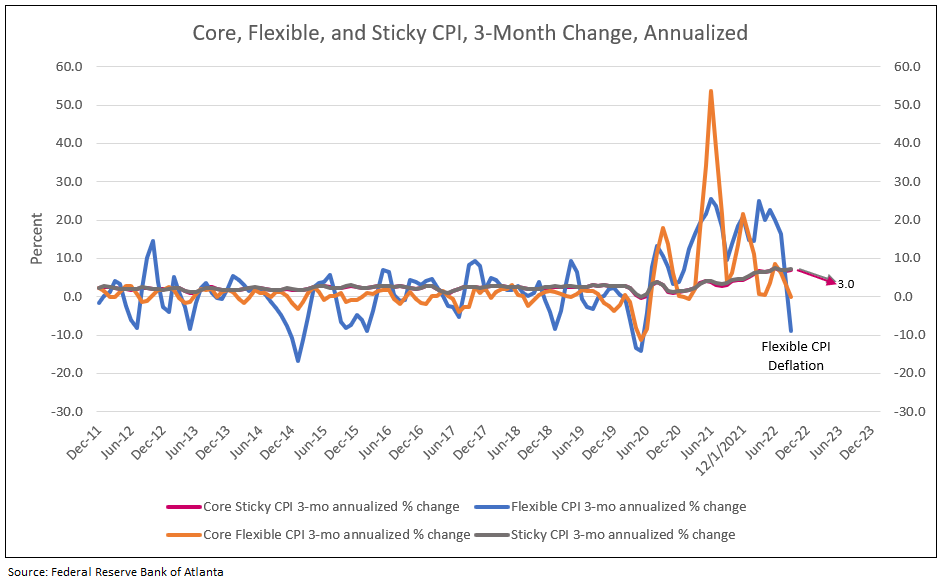

The percent change in flexible 3-month price has been decelerating since early 2022. The change in core flexible 3-month price is also falling. The sticky and core sticky 3-month rate of change peaked in 2022 and forecast to decelerate to 3% by mid-year 2023 (see Chart IV).

Chart IV

All Measures of Inflation Peaked in 2021 and Early 2022

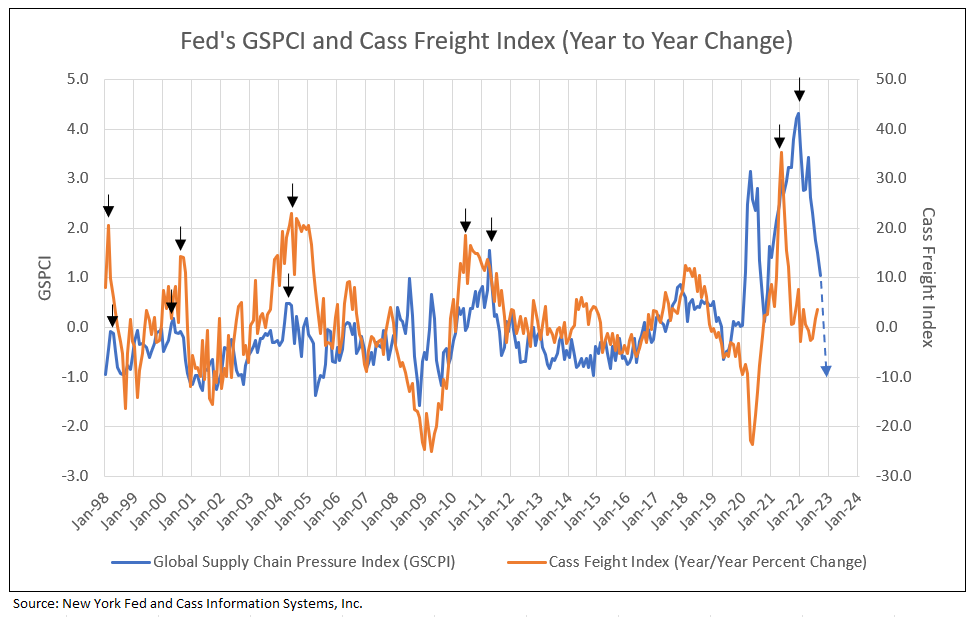

Cass Freight Leads the Fed’s Global Supply Chain Pressure Index (GSPCI) Forecasting Deflation from the Supply Chain in 2023

The regional banks’ Global Supply Chain Pressure Index incorporates data on shipping costs, delivery times, backlogs and other statistics, to create a single measure that can be compared with historical norms.

Another leading indicator, the Cass Freight Index, declined to zero seven months ago, forecasting a drop in GSPCI. By year-end 2022, the GSPCI is expected to decline from 1.0 in September to -1.00, indicating deflation from the supply chain in 2023 (see Chart V).

Chart V

Deflation from Supply Chain in 2023

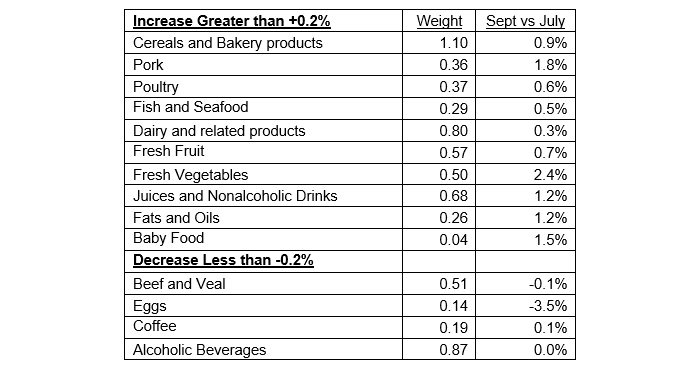

Food Price Increases Expected to Moderate

While food prices in September were up 0.8% compared to August, the combined weight of Food in the CPI is 13.6%. Food at Home was up 0.7% month-to-month, while Food Away from Home rose 0.9%.

Table I

Food at Home Percent Change Month-to-Month

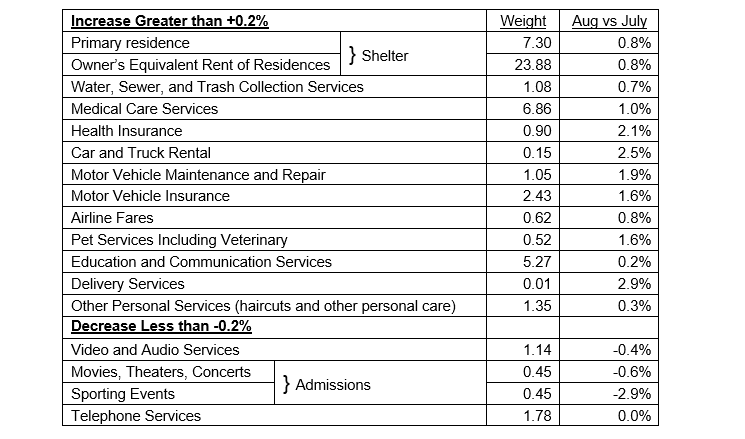

Service Inflation Decelerates in Coming Months

Services less energy services weight is 56.8% of CPI and rose 0.8% in September compared to 0.6% in August. The heavyweight is Shelter at 32.5% was up 0.7% in September. Medical and Educational Services has a weight of 6.9% and rose 1.0%.

As discussed later in details, shelter is a lagging price calculation determined from housing indicators 17 months ago without the impact of current housing and rent price indicators. The peak in year-over-year shelter inflation occurred in September 2022 and, with the subsequent decline in HMI from 90 in November 2020 to 46 in August 2022, forecasts 2.5% shelter inflation by December 2023 (see Charts IV and V).

Table II

Services Percent Change Month-to-Month

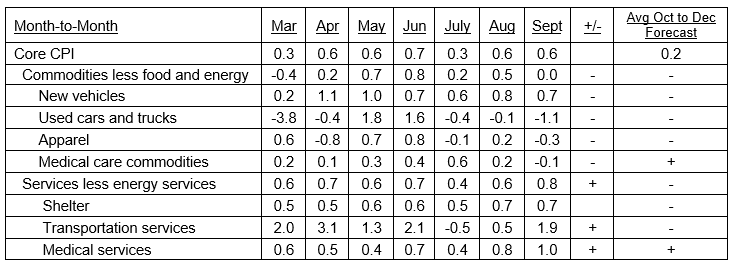

Table III

Percent Change in Core CPI for All Urban Consumers

“The Absolutely Ridiculous Inflation Measurement” – Jeremy Siegel

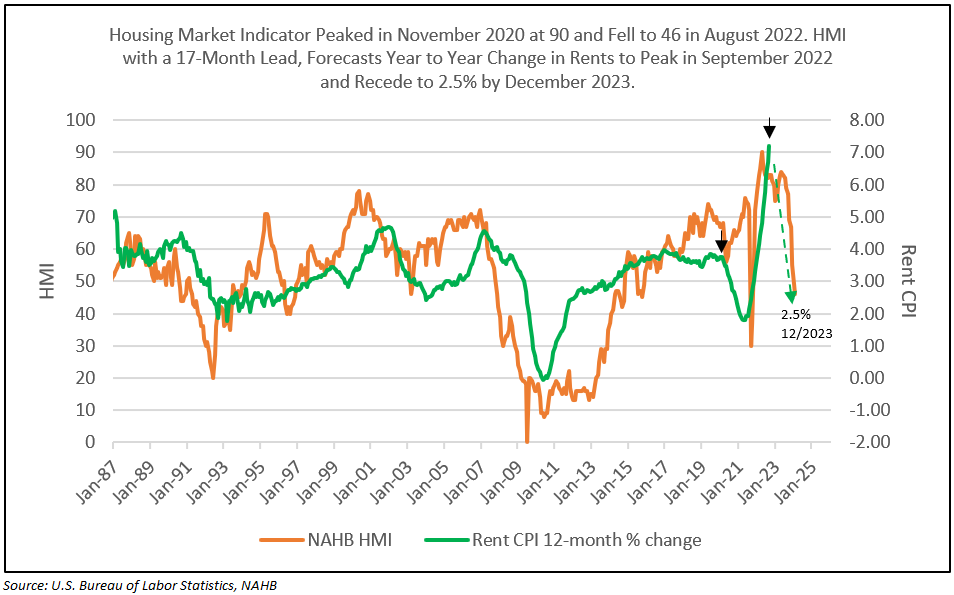

The Sticky Component of Rent, a Lagging Indicator, Will Retreat from Over 6.7% to 2.5% in December 2023

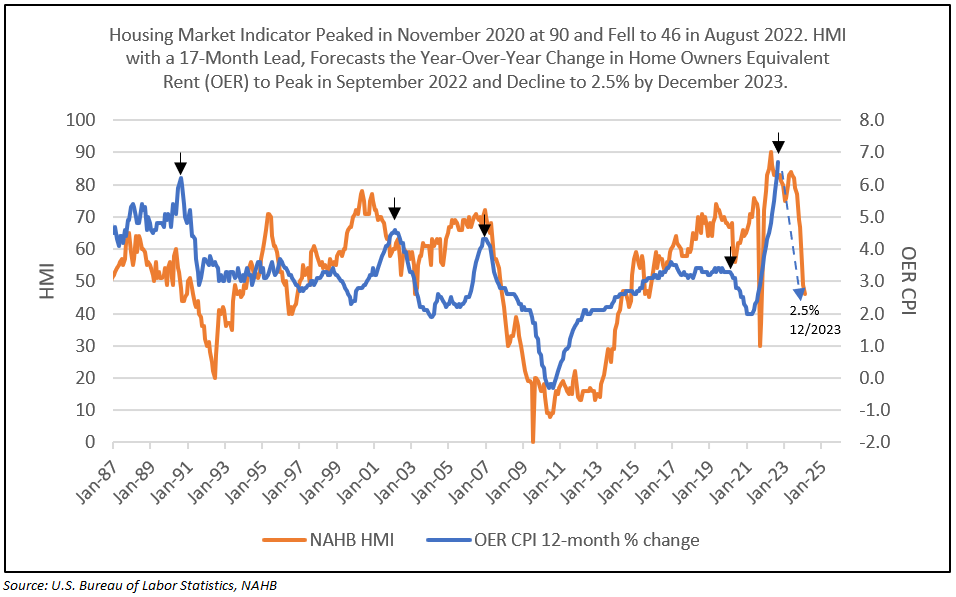

Rent component is measured by rent from primary residence (7.3% of CPI) and owners’ equivalent rent (OER, 23.8% of CPI) for a total of 32.5% of CPI, and 41.6% of Core CPI. Rent and OER are best forecast by the NAHB/Wells Fargo Housing Market Index (HMI) with a 17-month lead time.

HMI is based on a monthly survey of NAHB members designed to take the pulse of the single-family housing market. The survey asks respondents to rate market conditions for sale of new homes at the present time and in the next six months, as well as the traffic of prospective buyers of new homes.

HMI peaked in November 2020 at 90 and fell like a rock to 46 in August 2022. With the 30-year mortgage rate increasing to 7%, a further decline in HMI is projected for September. Plotted 17 months forward, HMI forecasts year-over-year monthly change in rent and OER. As a result, the sharp declines in HMI in 2022 with a 17-month lead time forecasts 2.5% rent and OER inflation in December 2023 (see Charts VI and VII).

Chart VI

Following the Lead of HMI, Rent Percent Change “Falls Like a Rock” in 2023 and 2024

Chart VII

Following a Decline in HMI, OER Percent Change “Falls Like a Rock” in 2023 and 2024

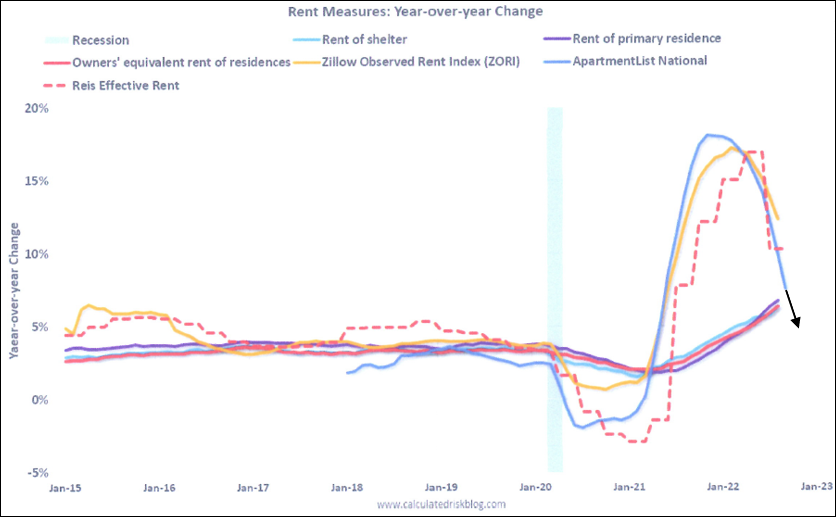

The rapid deceleration in current prices of rent and shelter assist in forecasting the rapid decline in the CPI rent components in 2022 and 2023.

Chart VIII

Rent Indicators Decelerate3

Short Term Implied Inflation

IDC uses a family of inflation indexes

- 1 Year Expected Inflation (INFL 1Y): Expected inflation over the next 12 calendar months (i.e., the market implied expectation for realized inflation over the course of the next year, starting from the latest published CPI).4

- 4 Year Expected Inflation, 1 Year from Now: Expected longer term inflation in one year’s time (i.e., the market implied four-year inflation expectation one year forward)

- 5-Year Implied Inflation: The market implied five-year market inflation expectation from today.

- 10-Year Implied Inflation: The market implied ten-year market inflation expectation from today.

- 5 Year Expected Inflation, 5 Years from Now: Expected longer term inflation in five years’ time (i.e., the market implied five-year market inflation expectation five years forward).

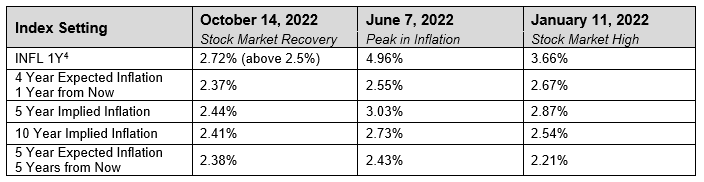

Inflation Expectations

Current indicative values for Inflation Expectations Indexes can be found in the table below, set alongside historical indicative data points from June 7 and January 11 of 2022.

Table IV

Current indicative values for U.S. Dollar Inflation Expectations Indexes

How much Reduction in Inflation is Sufficient to Meet the Fed’s Target?

The only inflation target we hear about from Fed speak to the media is to drive core PCE to 2%, yet the best measure of inflation remains levels implied by the bond market.

Implied inflation is a bond market measure.

- The 5-year T-Note yield less the 5-year inflation-indexed yield.

- The 10-year T-Note yield less the 10-year inflation-indexed yield.

- Five-year implied inflation 5-years-from-now (or 5-year minus 10-year implied inflation subtracted from the 10-year implied inflation rate, resulting in the implied inflation for the last 5 years of the next 10-year period.) Short-term implied inflation can also be measured over 1 or 4-year periods.

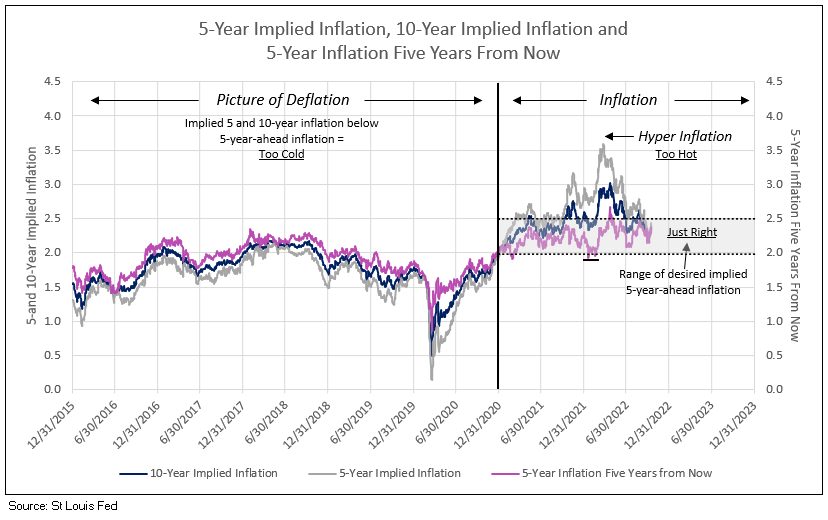

A picture of deflation.

Deflation is illustrated by measures of implied inflation, when the 10- and 5-year implied inflation rates are less than the 5-year rate 5-years in the future. Chart III illustrates the deflation that reigned from 2015 to 2020. The 5-year rate 5-years ahead remained slightly above and, at times, below 2%, while 5- and 10-year implied inflation continuously fell below this 5-year-ahead rate. The Fed does not desire any deflation outcome in the future.

A picture of controlled inflation.

Inflation is illustrated by 5- and 10-year implied inflation continuously greater than the 5-year-ahead rate. Levels of the 5- and 10-year implied rates above 2.5% are excessive and require Fed action, by both their media campaign and actions of the open market committee.

Implied inflation by all measures tumbled in the first half of 2022. Five and 10-year yields fell to 2.5% and the 5-year-ahead rate dropped to a little over 2%. However, today the 1-year implied inflation is at 2.72%, while 5-year is at 2.44%, 10-year is at 2.41%, and 5-years-ahead inflation rate is at 2.38%.

The increase in the UK Gilt yield raised the U.S. T-Note yield to levels that tighten liquidity beyond Fed requirements. A low in the British pound to the dollar and peak in UK Gilt yields continue to reflect an altered policy by the UK government.

Chart IX

All Implied Inflation Readings Decline to Acceptable Levels

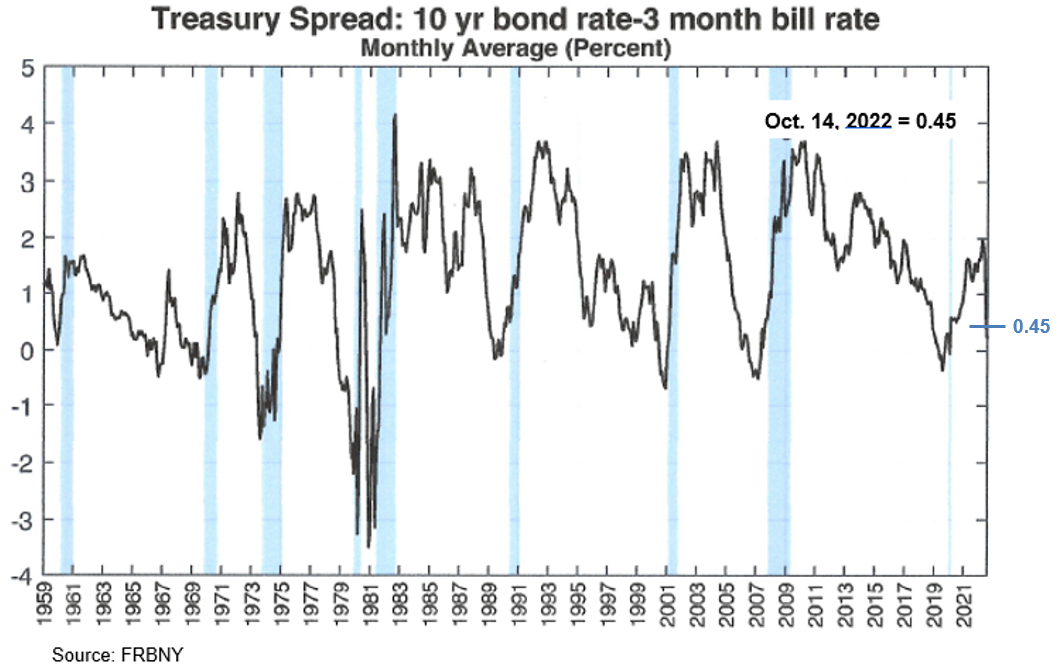

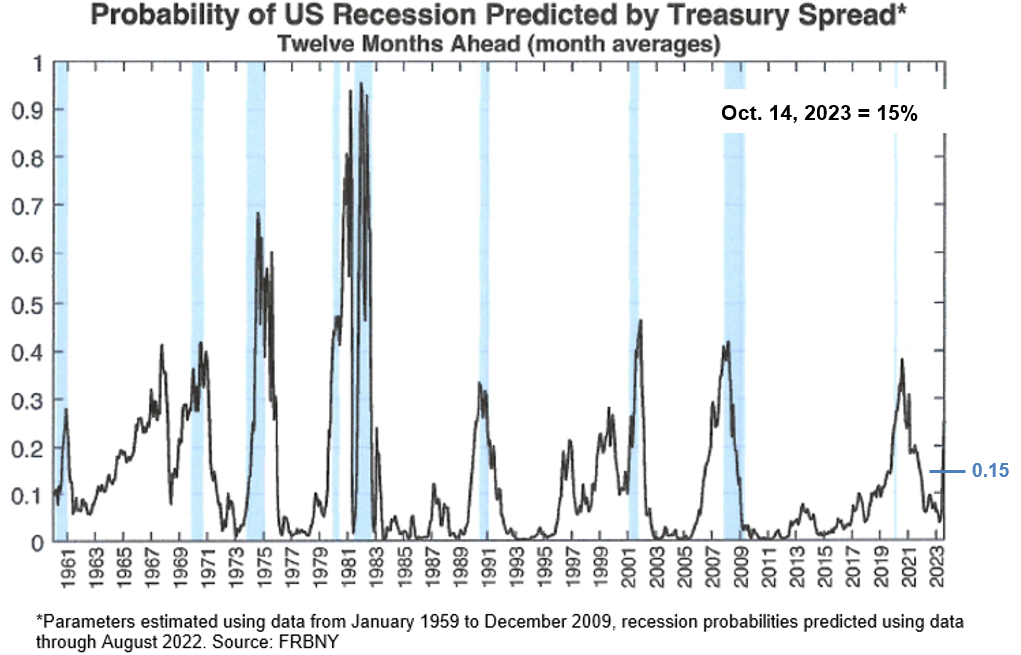

The Yield Curve as a Predictor of Recession Forecasts Low Probability of Recession in 20235

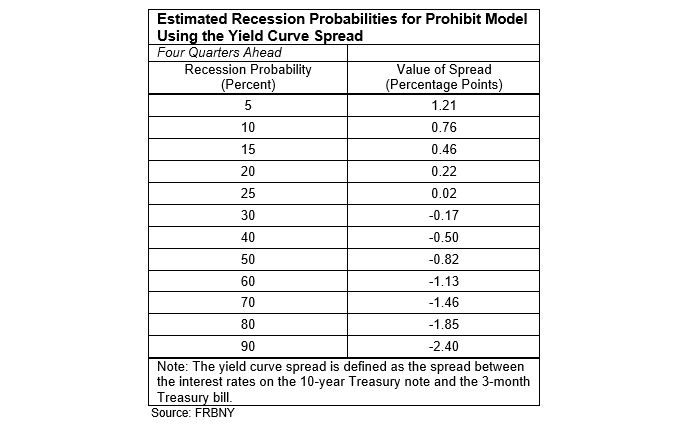

The Federal Reserve Bank of New York in a June 1996 study noted “one of the most successful models in our study estimates the probability of recession four quarters in the future as a function of the current value of the yield curve spread between the 10-year Treasury note and the 3-month Treasury bill.”

This current critical yield spread is 45 basis points, indicating a 15% probability of recession. In the recent past the spread ranged from 46 to 76 basis points, forecasting a 10 to 15% probability. The spread would be required to turn negative to reach a 30% or higher probability of recession one year ahead in 2023 (see Table V).

Table V

Chart X

Chart XI

Buy Equities

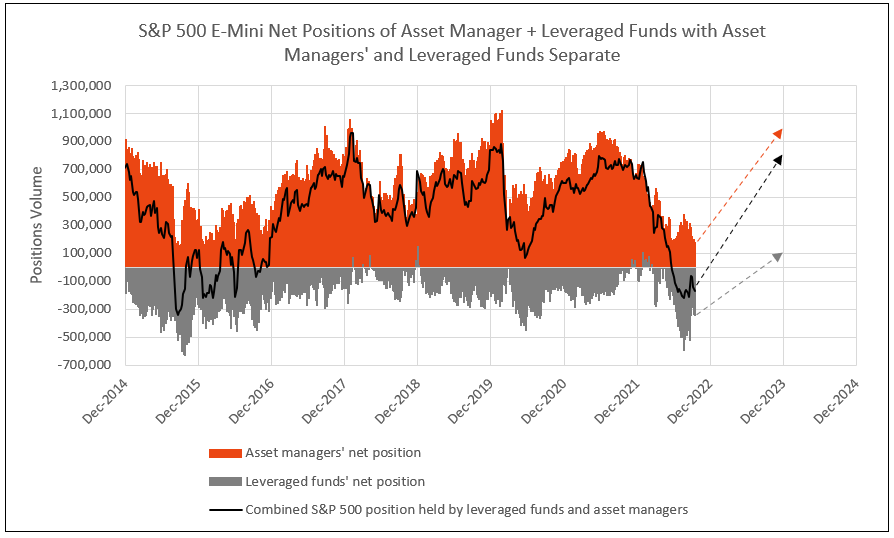

The past recommendation was to buy equities on weakness. The fears of inflation and the Fed’s actions, both in open media campaigns from Fed Chairman Powell, other regional presidents, and actions of the open market committee, together, created fear of a potential recession, driving stocks into a bear market in the first half of 2022, leading to a cycle low on June 16. Asset managers represented their bearish view by reducing net long positions in the Mini S&P 500 futures from almost 1 million in mid-2021 to 200,000 in June 2022.Leveraged funds increased the net short Mini S&P 500 futures position from zero at year-end 2021 to a record short position in August 2022, equal to the September 2015 levels. In September 2023, the leveraged funds reduced the net short position in half, a bullish trend (see Chart XII).

The levels of 1 million for asset managers and zero or higher for leveraged funds called the market peaks in February 2018, February 2020, and year-end 2021. The max negative levels of net short positions for leveraged funds called the stock market cycle lows in 2015, 2018, 2020 and especially in August 2022 (see Chart XII). In most cases, the cycle low in asset managers’ net long positions matches the extreme negative net short positions of leveraged funds. Note, however, asset managers’ positions bottomed following the June stock market low but leveraged funds did not reach its record low until mid-August 2022.

The record low in negative leveraged fund net short positions in September 2015 did not reach zero until February 2018 (a 3-year bull market). The next major net short low in the second quarter of 2020 did not reach zero until the end of 2021 (a 21-month bull market). The recent major low and reversal in leveraged fund positions forecasts a potential for a bull market in equities through 2023 (see Chart XII).

Chart XII

1 Tom Lee, Fundstrat, October 14, 2002

2 Tom Lee, Fundstrat, October 14, 2002 and New York Federal Reserve

3 Calculated Risk blog

4 ICE Inflation Expectation Index

5 New York Federal Reserve

Let IDC provide you the value and financial history of your favorite bank stock. For you to better understand our process of valuation, we offer a free, one-time analysis of one of the 202 banks in our bank analysis database. Simply send your request with the bank stock symbol to info@idcfp.com.

To inquire about IDC’s valuation products and services, please contact jer@idcfp.com or info@idcfp.com or call 262-844-8357.

John E Rickmeier, CFA

President

Robin Rickmeier

Marketing Director