Economist Campbell Harvey Says His Indicator That Predicted Eight US Recessions Is Wrong This Year

The following article, published by Bloomberg on January 4, 2023, sums up well the unique factors in today’s economy with inverted yields have led to a false recession signal.

Key Takeaways

- Everyone using the yield curve as a predictor forecasts recession in 2023.

- Normally, the spread of the 3-month T-Bill to the real 10-year TIPS yield parallels the spread of the 3-month to the nominal 10-year, forecasting a recession if the yield curves are negative.

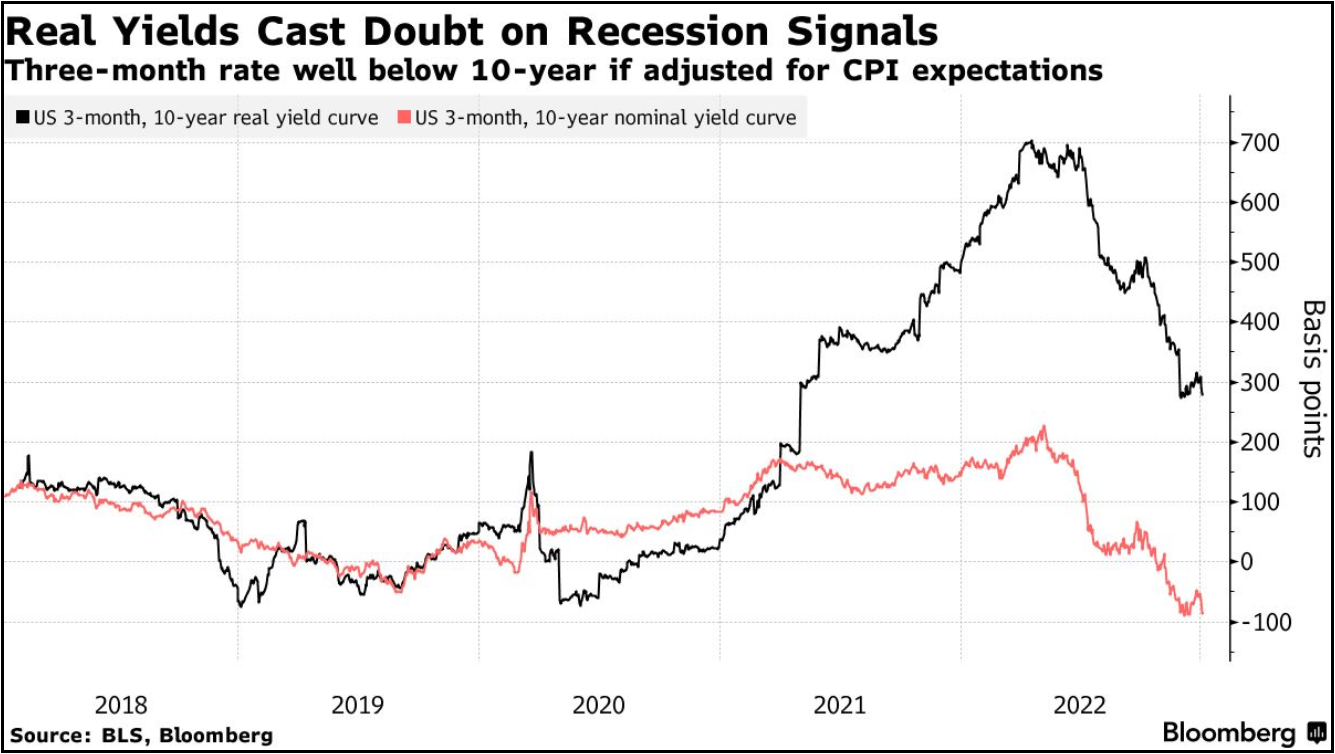

- In 2022 and 2023, the situation is different with the 3-month to 10-year real yield curve not confirming the negative 3-month to 10-year nominal yield curve (see Chart II).

- Conclusion: No recession or rolling recession by industry and positive GDP growth.

Economist Campbell Harvey has had a winning track record since he showed in his dissertation at the University of Chicago decades ago that the shape of the bond yield curve was linked to the path of US economic activity.

US recessions have been preceded by an inverted yield curve — when short-term rates exceed those of longer tenors — since the late 1960s. Fast forward to 2023, that’s exactly what’s been happening with the Treasury yield curve in the past month and half. Yet, Harvey is saying this time the US economy will manage to avoid a real slump even though it will keep slowing down for a bit longer.

“My yield-curve indicator has gone code red, and it’s 8 for 8 in forecasting recessions since 1968 — with no false alarms,” Harvey, now a professor at Duke University’s Fuqua School of Business, said in a interview Tuesday. “I have reasons to believe, however, that it is flashing a false signal.”

The spread between three-month rates and 10-year yields dropped to nearly minus one percentage point last month from as high as 234 basis points in May 2022. The spread, which Harvey’s work is based on, has been consistently inverted since mid November and hovered Wednesday at around minus 82 basis points.

Chart I

Despite the curve being inverted for the ninth time since 1968, Harvey said it’s probably not a harbinger for a recession.

One of the reasons is the fact the yield curve-growth relation has become so well-known and widely covered in popular media that now it impacts behavior, he said. The awareness induces companies and consumers to take risk-mitigating actions, such as increasing savings and avoiding major investment projects — which bode well for the economy.

Another boost to the economy is coming from the job markets, where the current excess demand for labor means laid-off workers will likely find new positions more quickly than usual. In addition, he said, given the largest job cuts so far have been in the tech sector, those highly skilled recently fired workers are also not apt to be unemployed for very long.

‘Dodge the Bullet’

Harvey’s model was linked to inflation-adjusted yields, and he said the fact inflation expectations are inverted — meaning traders see price pressures easing through time — also eases odds for a recession ahead.

“When you put all this together it suggests we could dodge the bullet,” Harvey said. “Avoiding the hard-landing — recession — and realizing slow growth or minor negative growth. If a recession arrives, it will be mild.”

The level of real yields also casts doubt on the recession signal. US 10-year yields adjusted for inflation are likely well above corresponding three-month ones. While there are no three-month break-even rates, cross-referencing the latest annual CPI reading with one-year break-evens would return a negative real rate for the tenor, compared with 10-year real yields above 1.5%.

Chart II

Harvey’s view is not the consensus. Many Wall Street firms are calling for a recession sometime this year or early 2024 in the aftermath of the Federal Reserve’s most aggressive hiking campaign in decades to rein on inflation.

Former Fed Chair Alan Greenspan said Tuesday a US recession is the “most likely outcome,” a view also shared by former New York Fed President William Dudley.

If the US economy manages to avoid recession, for Harvey, that won’t mean his model is now debunked.

“In science we use models all the time, and they’re simplifications of reality,” he said. “And part of the skill of the scientist is to know when to deploy the model and when not to or, in other words, to know the limitations of the model. And maybe I’m in a good position of knowing the limitations, given that it’s my model.”

One wildcard, he said, is if it the Fed after being late to raise rates last year proves to push them too high.

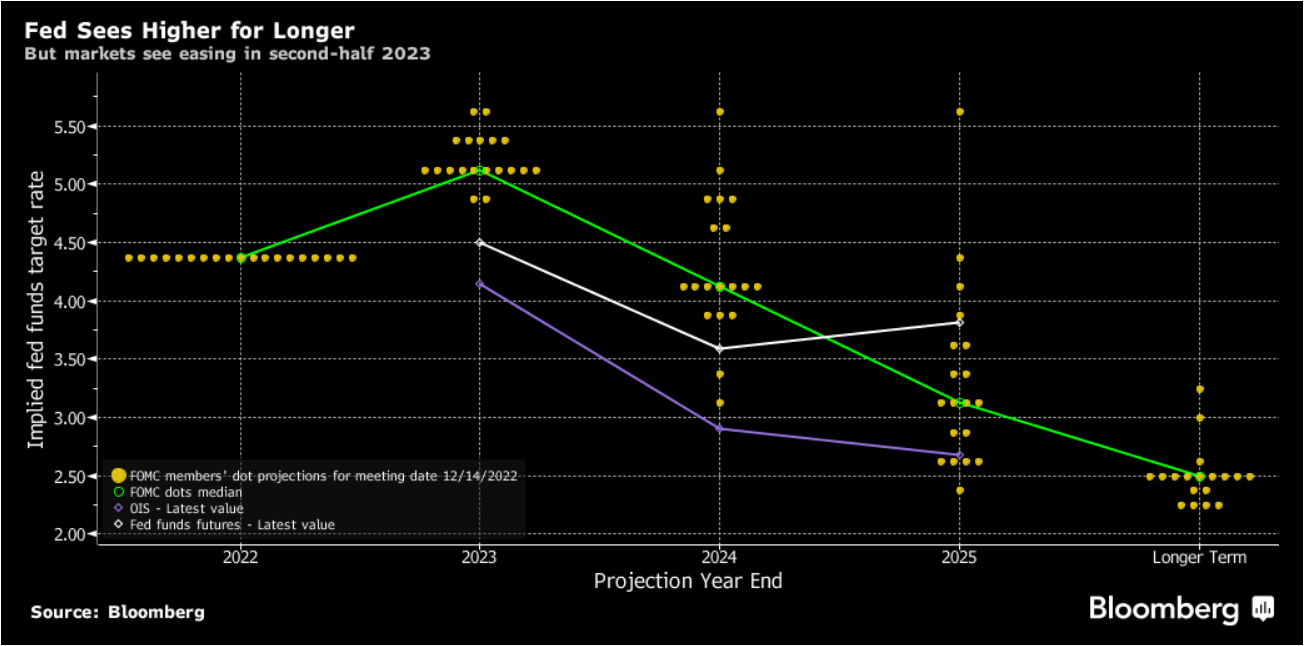

Chart III

Fed officials last month raised interest rates by half a percentage point, bringing their benchmark to a target range of 4.25% to 4.5%. Quarterly forecasts also released showed rates ending next year at 5.1%, according to their median forecast, with no rate cuts before 2024.

Fed policy makers in their gathering last month also affirmed their resolve to bring down inflation, according to minutes of the their Dec. 13-14 meeting released Wednesday.

“I believe the time to end the tightening is now,” Harvey said.

Source: Economist Says His Indicator That Predicted Eight US Recessions Is Wrong This Year, Bloomberg.com