Forecasting a Recession with the Sahm Rule

Forecasting a recession for a bank is key in determining the loan loss provision (predicting loan loss over the life of the loan) under CELA. As an example, JP Morgan Chase & Co, the biggest bank in the US, is setting aside more than $1 billion in preparation for potential loan losses.

Most economists predict a downturn in the US in 2024, as a result of the large hike in the Fed funds rate in 2022 aimed at combating inflation. Yet, economists, in the recent past, had noteworthy misses on inflation and GDP. This exercise is more akin to putting together the pieces of a puzzle, with each economic indicator filling in part of the image.

Right now, the pieces are not fitting together well. Manufacturing is in recession, and the housing market has declined significantly. Second quarter GDP was strong, showing that consumer spending (70% of GDP) remained resilient. More important, the October jobs report was weak with 150,000 new jobs reported and an unemployment rate of 3.9%.

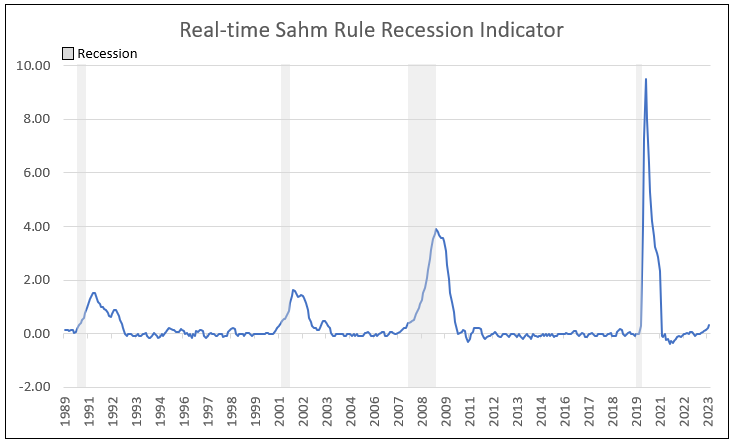

Claudia Sahm, the former Fed economist, came up with her own real-time recession test. Called the Sahm Rule, it signals the start of a recession when the 3-month moving average of the unemployment rate rises by 0.5% above the 12-month low of the unemployment rate. The unemployment rate was 3.4% in January and again in April, and increased 0.5% to a rate of 3.9% in October. In order to indicate the beginning of a recession, the unemployment rate would be required to report 3.9% or higher for two more consecutive months (see Chart I).

Chart I

On November 3, Claudia Sahm posted on X that while the unemployment rate reaching 3.9% is not good, the Sahm rule, currently at 0.33%, “did not trigger…nor is it right on the edge,” In addition, she states the rule has “triggered *within* 3 months of prior recessions.”

To view all our products and services please visit our website www.idcfp.com. For a copy of this article, please contact us at 800-525-5457 or info@idcfp.com.

John E Rickmeier, CFA

President

jer@idcfp.com

Robin Rickmeier

Marketing Director