Adequacy of Capital - - The “A” in CAMEL

IDC Financial Publishing, Inc. (IDCFP) uses the acronym CAMEL and its component financial ratios to evaluate the safety and soundness of commercial banks and savings institutions. This article explains how IDCFP uses the adequacy of bank capital as a component of its CAMEL ranking system and why it is valuable and important to monitor.

The adequacy of capital is defined by IDCFP as the adjusted Tier 1 capital ratio. To calculate, subtract from the Tier 1 capital ratio 90 days past due loans, nonaccrual loans and repossessed assets, and net of the loan loss reserve, all as a percent of Tier 1 capital. Given the percentage of delinquency and other bad loans net of the loan loss reserve, reduce the reported Tier 1 capital ratio – the higher the risk of bank failure.

An adjusted Tier 1 capital ratio below 5% indicates insufficient capital and loan loss reserves to cover delinquency, nonaccrual loans and repossessed assets and an IDCFP rank less than “125” (300 the Highest and 1 the Lowest).

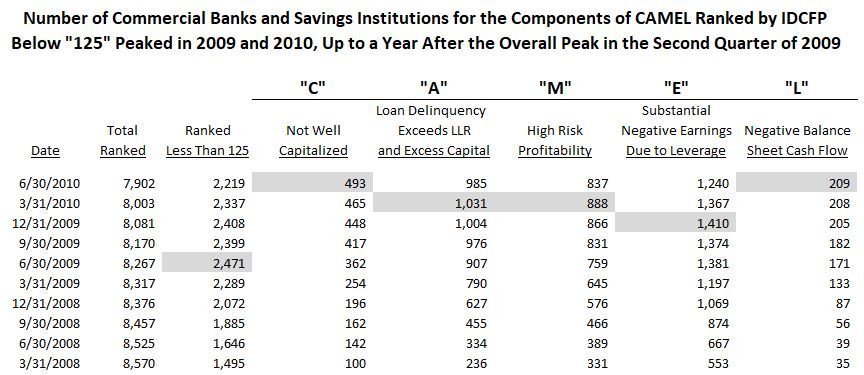

As seen in the table below, the number of commercial banks and savings institutions, ranked less than the industry standard of “125”, peaked in the 2nd quarter of 2009 at 2,471 or 31% of the 8,237 total number of domestic commercial banks and savings institutions. The number of commercial and savings banks, however, flagged by IDCFP as not adequately capitalized, as defined above by adjusted Tier 1 capital, peaked at 920 three quarters later ending on March 31, 2010.

Other rating agencies that primarily depend on loan delinquency and other forms of bad loans in determining their ratings are late in identifying risk and only recognize a portion of the high-risk banks and savings institutions. As witnessed in IDCFP’s CAMEL analysis, categories of CAMEL with their rank calculations lag behind the timely and unique combination of these components in the IDCFP summary rank of financial ratios.

This illustrates that all 5 categories of rank, C-Capital, A-Adequacy of Capital, M-Margins as a Measurement of Management, E-Earnings from Operations and, separately, Earnings from Financial Leverage, and finally, L-Liquidity all together provide a timely indication of risk and potential failure.

Most important, the number of banks and savings institutions with IDCFP ranks below “125” began sharply increasing after the 2nd quarter of 2006, well before the financial crisis of 2008 and 2009.

IDCFP has been helping CD brokers and investors, insurance companies, federal agencies, numerous state governments and a host of other institutions make better decisions using its unique and proprietary CAMEL rating methodology since 1985. For more information on CAMEL go to www.idcfp.com or call 1-800-525-5475.