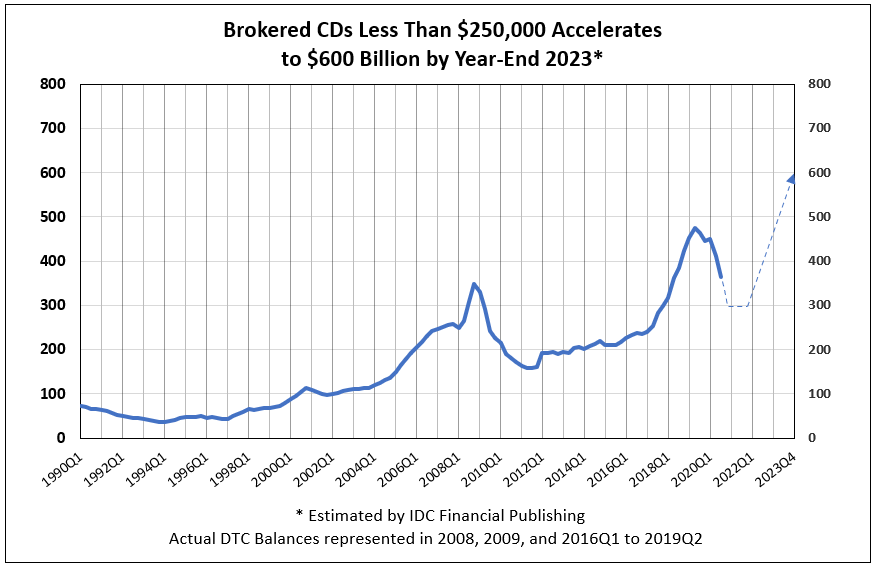

Insured Brokered CDs to Increase 64% to $600 Billion by Year-End 2023

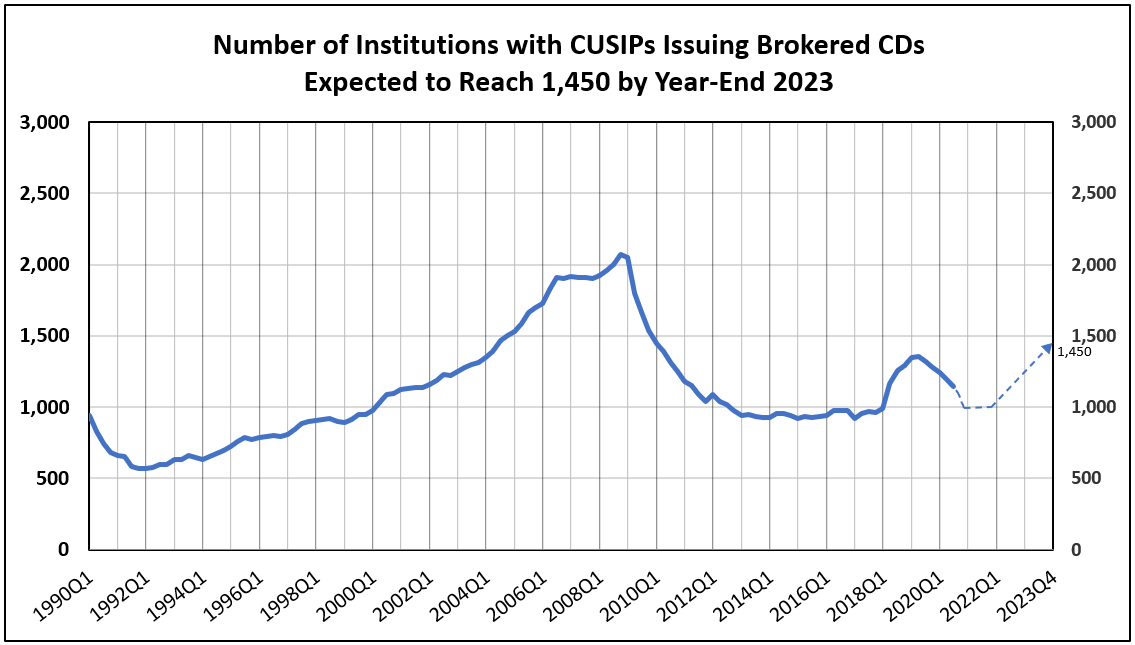

The Number of Financial Institutions Issuing Brokered CDs Temporarily Declines

The number of institutions issuing brokered CDs grew significantly in 2018 and 2019. Banks, savings institutions, and credit unions rose from a plateau of 961 in 2017 and increased to a peak of 1,356 in the 2nd quarter of 2019.

The subsequent decline was due to, first, the rise in the federal funds rate to 2.5% at year-end 2018, maintaining that rate above other short-term yields, and raising interest rates on brokered CDs above other deposit rates and short-term T-Bill and T-Note yields in 2019. As a result, the growth in the number of institutions issuing brokered CDs less than $250,000 slowed to 1,278 by year-end 2019. Second, the advent of Covid-19 in the first quarter of 2020 reduced short-term US Treasuries to zero, as the Federal Reserve stimulated the economy. As a result, financial institutions issuing brokered CDs fell to 1,141 by the end of the third quarter.

At IDC Financial Publishing (IDCFP), we project a future resumption of growth in the total value of brokered CDs less than $250,000. The number of institutions issuing these CDs is expected to decline to 1000 for year-end 2020 and remain there through 2021. Then, following economic recovery from Covid-19 and a more positive yield curve, the forecast for the number of institutions issuing these CDs to rise again, reaching 1,450 by the end of 2023 (see Chart I & II).

Chart I

Chart II

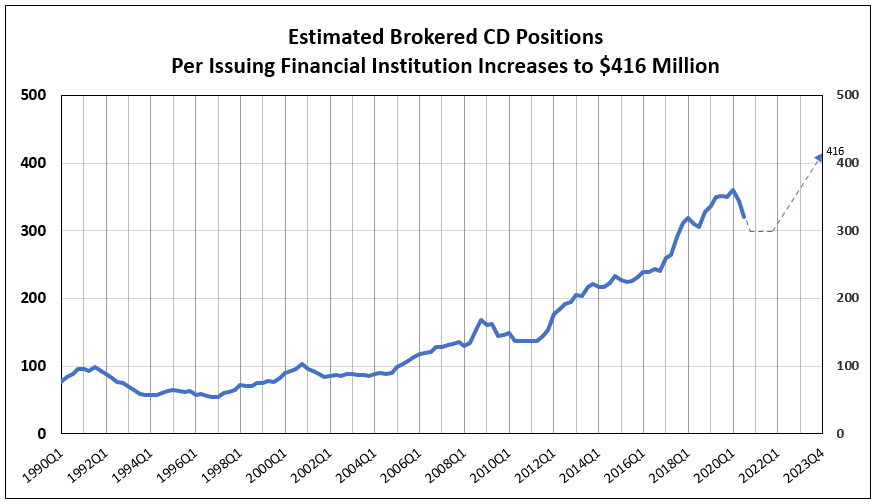

The Value of Brokered CDs per Issuing Institution Continues to Rise on Trend

The value of brokered CDs issued per financial institution grew exponentially over the last two decades, due to an increase in government insured levels to $250K, bank mergers, and strong growth in loans for those core banks and credit unions issuing brokered CDs. The value grew from an average of $78 million in 1999 to a peak of $360.6 million by the 1st quarter of 2020.

Each quarter, IDCFP estimates the total value of brokered CDs less than $250K and divides it by the total number of financial institutions issuing these CDs. This determines the estimated average value of insured brokered CDs per issuing financial institution. In the 4th quarter of 2008, the average value peaked at $166 million, and then fell to $137 million in 2010, due to the banking crisis. Since then, the value per institution has risen, reaching a peak of $361 million in the 1st quarter of 2020. With the advent of Covid-19 and near-zero short-term treasury yields, brokered CDs per issuing bank fell to $319.8 million as of September 30th, 2020 and estimated to fall again to $300 million with the release of 2020Q4 reports and remain at $300 million in 2021. However, with economic recovery in 2022 and 2023, the forecast of this future dollar growth will be $14.5 million per quarter, reaching a record average of $416 million by year-end 2023 (see Chart III).

Chart III

Growth in Outstanding Brokered CDs Forecast at $37 Billion a Quarter in 2022 and 2023

Following economic recovery from Covid-19, stimulus from Federal spending, i.e., infrastructure spending, and other government initiatives, will supplement the increase in private spending. As forecasted by the Federal Reserve, GDP growth is expected to expand to 4.2% this year, 3.2% in 2022, and 2.4% in 2023. This, in turn, will create bank lending, as the U.S. 5-year yield continues to rise toward 1%, and increase the number of financial institutions issuing brokered CDs. Currently, outstanding brokered CDs account for 30% of their time deposits, up from 19% in the 4th quarter of 2008. This percentage has grown on trend from 2008 to 2019 but is expected to level off at 30% through year-end 2023.

To forecast growth of DTC brokered CDs outstanding, we multiply the number of commercial banks, savings institutions, and credit unions with outstanding brokered CDs, times our estimate of the average of insured brokered CDs per issuing financial institution. Though we expect total brokered CDs will continue to decline to $300 billion and remain there through 2021Q4, we anticipate a reversal and that number to double by year-end 2023.

Following economic recovery, we forecast DTC brokered CDs outstanding to increase 64% from the reported $365 billion at quarter-end 2020Q3 and reach $600 billion by year-end 2023 (see Chart IV).

Chart IV

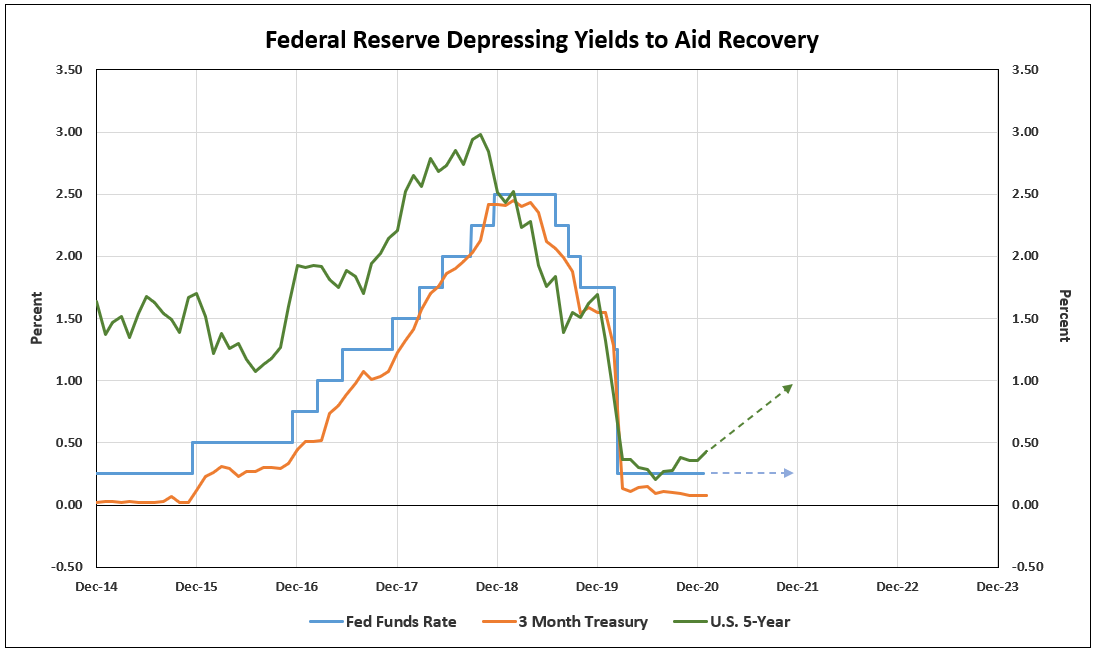

The Federal Reserve Policy into 2023 Remains Depressing Short-Term Yields to Aid in Economic Recovery

The 5-year nominal U.S. Treasury is the basis for pricing the long end of 3 to 5-year maturity ladder for brokered CDs $250,000 or less. Over the next two years, yields are projected to increase following the control of COVID-19 and with economic recovery. To avoid the decline in bond prices as yields rise, investors buy CDs, staggering maturities over years in a maturity ladder.

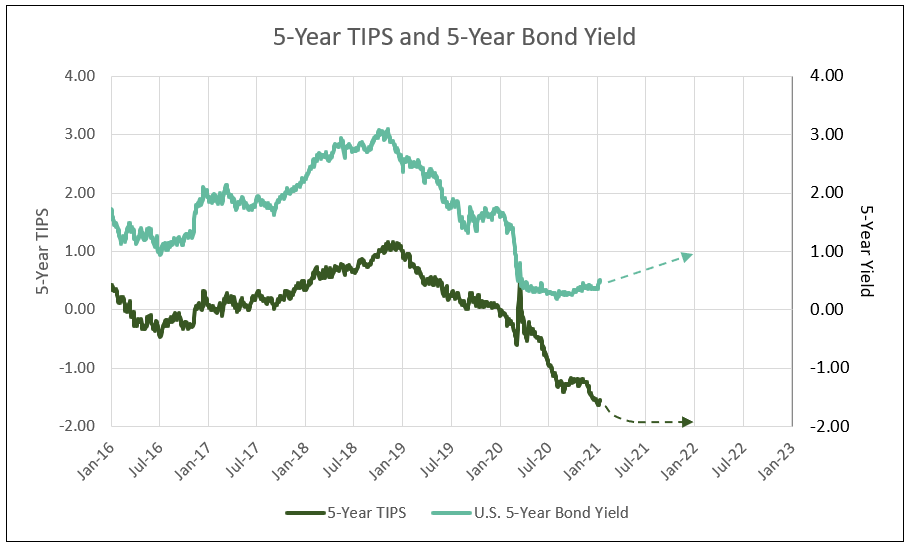

However, to get an increase in the nominal 5-year yield, the Fed needs to step aside from buying these bonds, which holds down the yield. Evidence can be seen in the continuous decline in the yield on 5-year TIPS (Treasury Inflation-Protected Securities). The continuous decline to -1.7%, with a stable nominal yield at 0.5% due to Fed buying, creates a spread which is the inflation expectation (the 2.1% difference between the 5-year nominal yield and 5-year TIPS). Despite the increase in anticipated inflation, the nominal yield remains flat around 0.5%, forcing the TIPS to new lows. Brokered CDs will again become attractive once the nominal yields rise to 1% to 1.5% and the TIPS yield stabilizes or increases (see Chart V).

Chart V

For further information or to view our products and services please visit our website www.idcfp.com or contact us at 800-525-5457 or info@idcfp.com.

John E Rickmeier, CFA, President, jer@idcfp.com

Robin Rickmeier, Marketing Director