German 3-Month Yield Spikes to a Low, Approaching the Record Low from December 2017

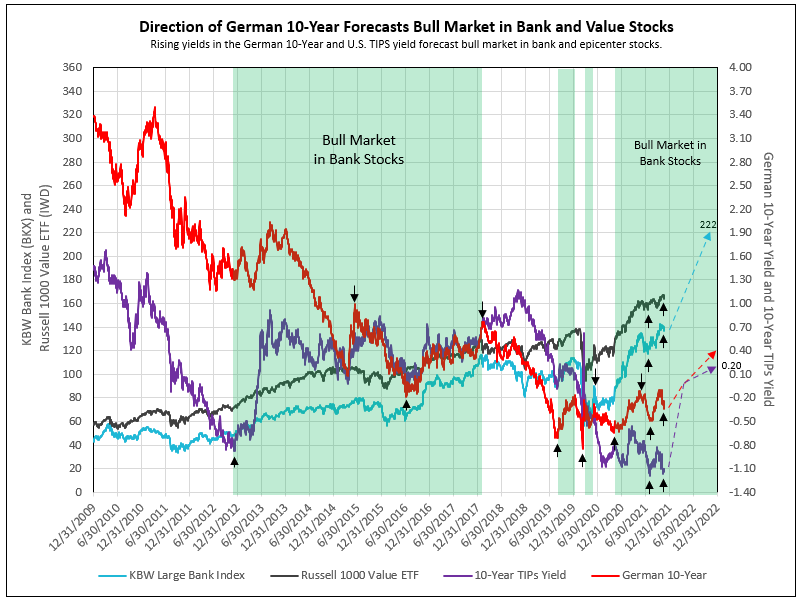

Following is an update to IDC’s article “How the German 10-Year Yields Forecast the Beginning and End of Bull Markets in Bank and Value Stocks,” where the research indicated the U.S. 10-year TIPS yield, combined with the German 10-year, forecast two major bull markets in bank stocks, from December 10, 2012 to February 15, 2018, and from October 29, 2020 to-date, and into 2022.

This article also provides an update to our article from November 2nd, observing how spike lows in the German 3-month yield and the steepening of the German short-term yield curve forecasts cycle lows in the German DAX and S&P, as well as how short-term German yields assist in forecasting cycle lows in bank stocks. In addition, we detail how the fundamentals of banks’ operating and financial returns, combined to equal ROE, demonstrate the superior performance of bank stocks in the two major bank stock bull markets in the last decade (from December 2012 to February 2018 and from October 2020 to today and into 2022).

Steepening of the German Short-Term Yield Curve Forecasts Cycle Lows in DAX, S&P 500 and Bank Stocks (BKX)

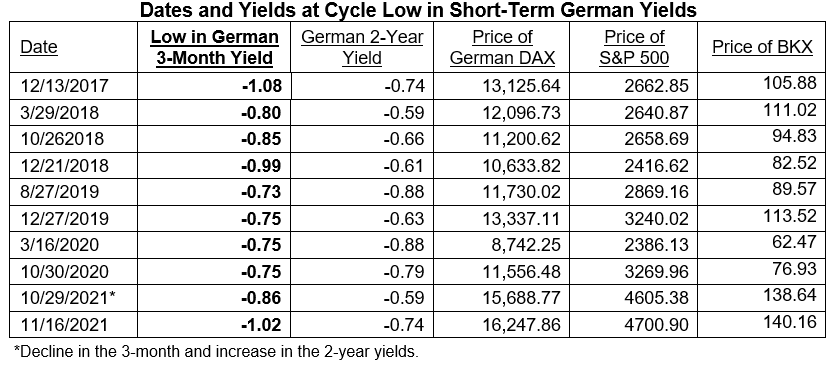

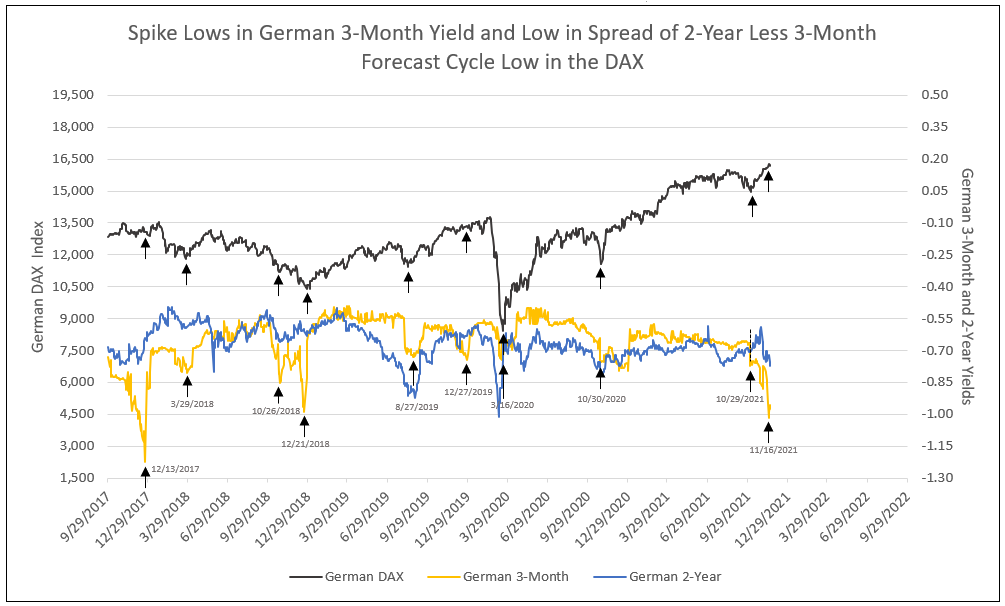

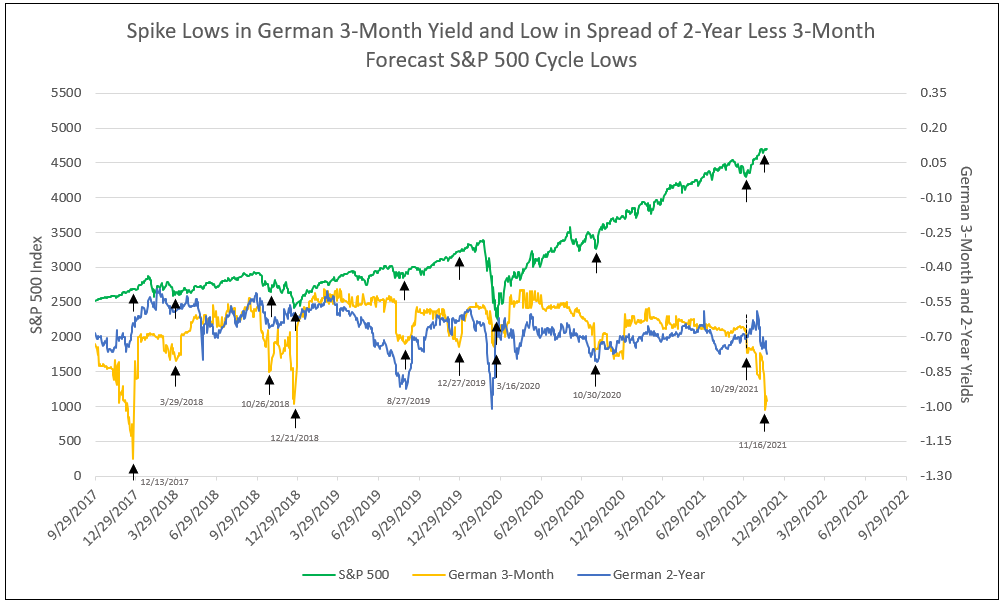

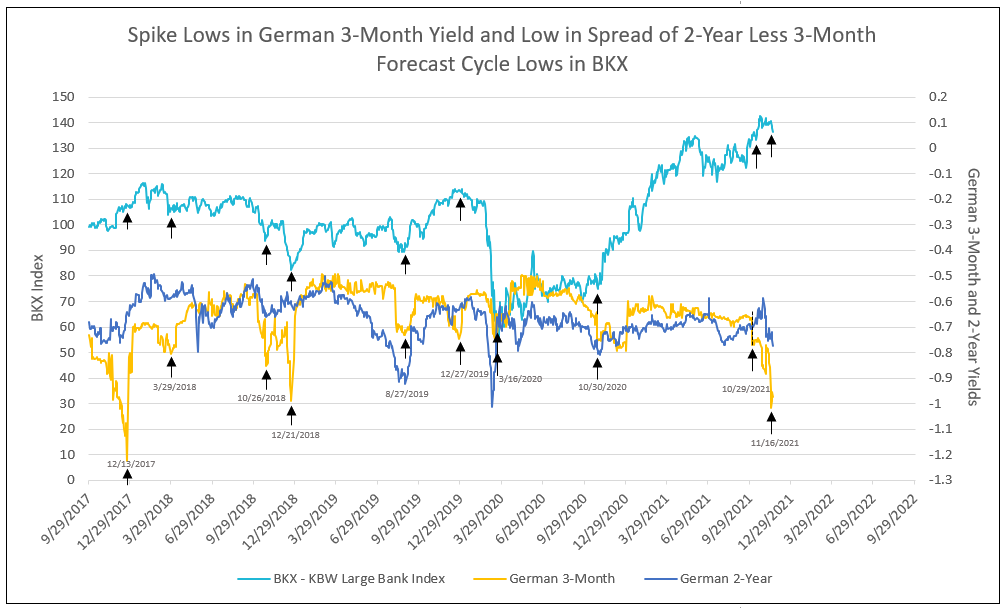

In Germany, the 3-month yield periodically spikes to a low, steepening the German yield curve relative to a lesser decline in the German 2-year yield. Historically, the German 3-month yield declined to negative values beginning year-end 2015. Subsequently, a spike low in the German 3-month yield below -0.70% or more has called short-term cycle lows in the DAX (see Chart I), the S&P 500 (see Chart II), and the KBW Large Bank Index (see Chart III).

The Bundesbank of Germany relies on a steepening yield curve to stimulate its economy. The Federal Reserve, on the other hand, limits the low in the Fed funds rate to zero. When the German 3-month yield spikes a low below -0.70% this signals a steepening yield curve in Germany, and further translates to a cycle low in the German DAX, the U.S. S&P 500 and BKX bank indices.

The ability for a spike low in the German 3-month to forecast the S&P 500 and bank stocks relates to interest rate arbitrage between Europe and the U.S. and the inter-relationships between the two economies. The correlation to market lows illustrates the point.

Table I

The most recent cycle low in the DAX, S&P 500 and BKX determined by the German 3-month and 2-year yields is different than in the past. Historically both German yields declined, with the cycle low in the 3-month signaling the low in the equity markets. On October 29, 2021, however, the 3-month fell significantly to -0.86%, while the 2-year rose to -0.59% from -0.67% a few days earlier. This fall in the German 3-month and rise in the 2-year created a spike low in the corresponding short-term yield spread and forecast the cycle low in equities (see Charts I, II and III).

Another spike low occurred on November 16, 2021, closing at -1.016, plus intraday lows of -1.023 on November 17 and 18. This was the lowest yield since the December 13, 2017, spike low of -1.08% (see Table I).

The Federal Reserve has a different problem, as it won’t allow negative short-term rates. Only the TIPS yields are negative. The U.S. yield curve rises from a zero Fed funds yield to the 30-year bond yield. The nominal yield curve is normally a positively sloping line with the short end currently held down by a zero Fed funds rate. Today, however, higher reported inflation is priced in implied inflation, which lifts yields along the curve, forcing TIPS yields to record negative levels, and causing distortions in yield spreads between various maturities.

As an example, current reported inflation recently increased 5-year implied inflation to 3.17%. Most of the increase was absorbed by a decline in the 5-year TIPS yield to -1.91%, and the remainder allowed for an increase in the 5-year nominal yield to 1.27%. A portion of expected inflation was also priced in the 10-year yields, but a smaller amount in the 20 and 30-year maturities. With nominal yields along the curve distorted by implied inflation, the yield spreads of the 30-less-10-year narrowed significantly, creating an illusion of a forecast for an economic slowdown. In reality, the economy is on the verge of significant expansion.

Chart I

Chart II

Chart III

Chart IV

Signals from the German 10-year yield and TIPS yields, coupled with the affirmation provided by cycle low spikes in the German 3-month yield, indicate buy and sell dates for the BKX, QQQ and S&P 500 indices (see Table II). The German 10-year yield peaked at -0.10 and temporarily retreated to -0.34% as Covid increased in Germany. With Covid peaking in the near future, the cycle low in the 10-year coupled with the low in U.S. TIPS yields forecasts continued strength in bank and value stocks (see Chart IV).

The average bank stock offers a 54% appreciation potential while the BKX (Large Bank Index) indicates a 60% potential. The first leg of the current bank bull market began October 30, 2020 with a spike low in the German 3-month yield. The second leg began August 4, 2021 with the cycle low in the German 10-year yield. Then, on October 29 and again from November 16 to 19, 2021 the lows in the German 3-month yield confirmed the second leg of the current bank stock bull market (see Charts III and IV).

See other recent articles published by IDC discussing how:

- Bank financial history illustrates a secular increase in profitability and

- The German 10-year forecasts bull markets in bank stocks.

To inquire about IDC’s valuation products and services, please contact jer@idcfp.com or info@idcfp.com or call 262-844-8357.

John E Rickmeier, CFA

President

Robin Rickmeier

Marketing Director